Executive Summary: Rigs: The total US rig count increased by 2 rigs W-o-W, up to 582 for the April 21 week from 580. Infrastructure: Upcoming maintenance work on the Wink-to-Webster and Midland-to-Echo III pipelines will send ripples through the crude oil market. Storage: East Daley expects an injection of 472 Mbbl in commercial and Strategic Petroleum Reserve (SPR) inventories for the week ending May 3.

Rigs:

The total US rig count increased by 2 rigs W-o-W, up to 582 for the April 21 week from 580. Liquids-driven basins increased by 1 rig W-o-W to a total of 476. The Permian and Uinta basins each added 1 rig, with the Permian’s add coming from the Midland. The DJ decreased by 1 rig W-o-W down to 8.

DJ operator Civitas Resources removed a rig, leaving 1 rig remaining. Permian Resources in the Midland and Rose Petroleum each added 1 rig W-o-W.

Infrastructure:

Upcoming maintenance work on the Wink-to-Webster and Midland-to-Echo III pipelines will send ripples through the crude oil market. East Daley expects to see a rerouting of some supplies from the Permian that will pressure Midland prices in June.

With 1.5 MMb/d of capacity, Wink-to-Webster and Midland-to-Echo III is a primary artery out of the Permian Basin to the Houston market. Wink-to-Webster has operated at a high throughput since start-up in 4Q20, moving an average of ~800 Mb/d in 2023. Combined with Midland-to-Echo III, the system ran ~1.2 MMb/d on average in 2023, or nearly 20% of Permian demand (~6.1 MMb/d in 2023. Enterprise Products (EPD) has an undivided joint interest in the system, making the aggregate capacity 1.5 MMb/d.

On its 1Q24 earnings call last Tuesday (April 30), Enterprise said it has notified shippers of the 10-day maintenance work, scheduled to begin in June. The work on the pipelines will force shippers to find alternative routes for ~1.2 MMb/d of Permian flows.

According to EDA’s Crude Hub Model, pipes to the Gulf Coast have ~937 Mb/d of excess capacity split between Corpus Christi, Houston and Nederland, based on average flows in 2023. Of this total, ~360 Mb/d is capacity to Corpus Christi and Nederland, so the majority of oil will still flow to Houston on less desirable pipes. For example, ONEOK’s (OKE) BridgeTex has ~360 Mb/d of excess capacity. However, due to its high ‘23 average blended rate ($2.04/bbl), the pipe is significantly underutilized.

In addition to these destinations, pipes to Cushing have spare capacity (~449 Mb/d) and could be a market of last resort. Barrels could flow north from West Texas to Cushing, then south towards the Gulf Coast. However, shippers would need to pay stacked rates well above the -$1.25/bbl spread currently.

The impact on shippers is unclear until actual nominations are made in mid-May. In response, producers could empty their storage tanks in May to maximize returns on current inventory and make space to refill in June while the pipe are down. The urgency is underscored by the June Midland – MEH spread dropping from -$0.40/bbl to below -$1.10/bbl.

Storage:

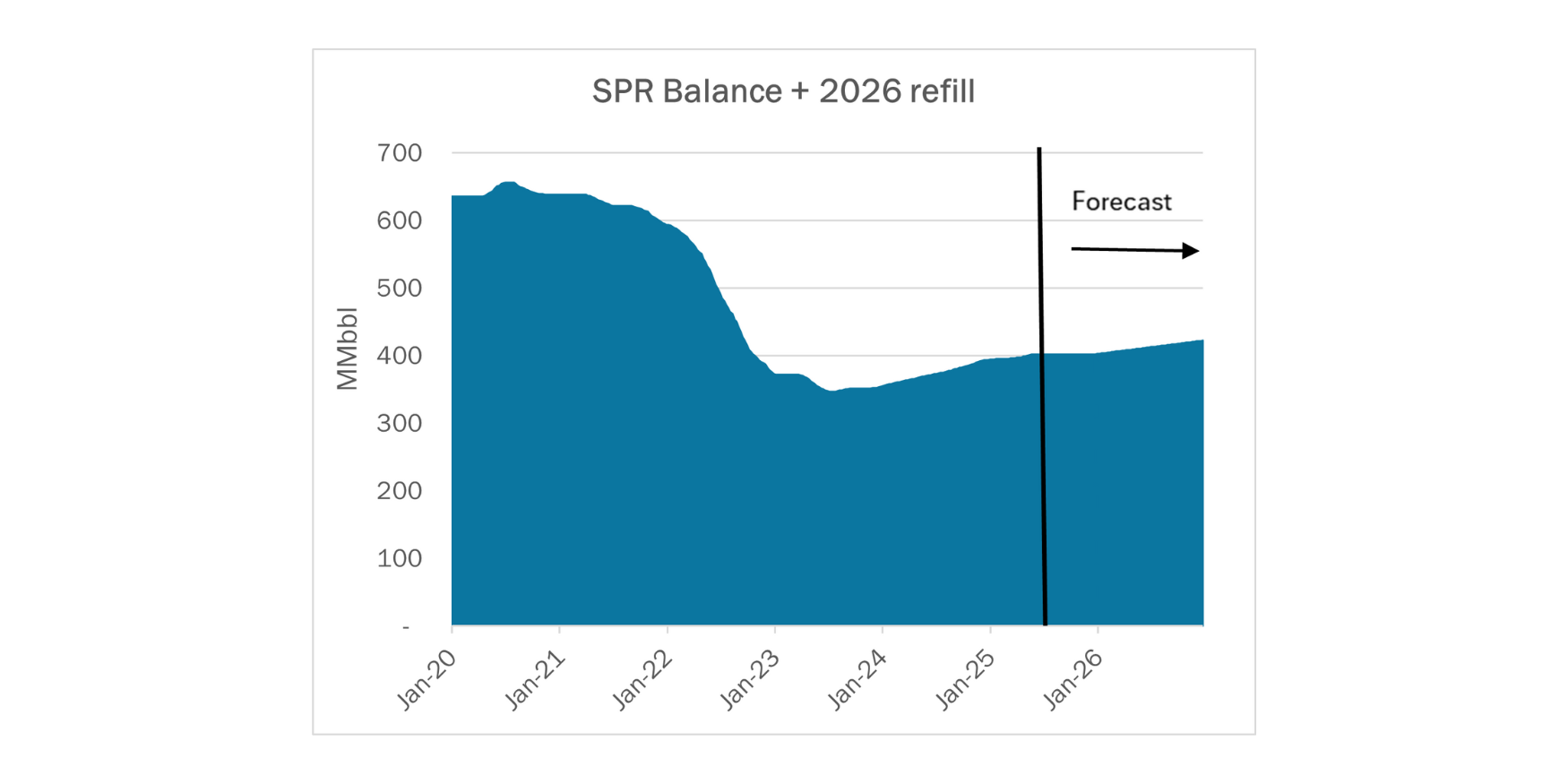

East Daley expects an injection of 472 Mbbl in commercial and Strategic Petroleum Reserve (SPR) inventories for the week ending May 3. We expect total US stocks, including the SPR, will close at 821 Mbbl.

The US natural gas pipeline sample, a proxy for change in oil production, fell ~5.6% W-o-W across all liquids-focused basins. Samples decreased 1.60% in the Williston and 7.27% in the Gulf of Mexico. The declines were offset by a 4.97% increase in the Eagle Ford, 0.18% in the Rockies, and 0.51% in the Permian. Both the Williston Basin and the Rockies have a very high correlation between gas volumes and crude oil volumes, whereas the Eagled Ford’s correlation is less than 30%. We expect US crude production to remain flat at 13.1 MMb/d.

According to US bill of lading data, US crude imports decreased by 116 Mb/d W-o-W to 6.6 MMb/d. More than 60% of the supply originated from Canadian pipelines into the US, with the remainder largely coming from ships carrying crude from Mexico, Brazil and Argentina.

As of May 3, there was ~955 Mb/d of refining capacity offline, including downtime for planned and unplanned maintenance. EDA expects gross crude inputs into refineries to increase by ~215 Mb/d W-o-W, coming in at 15.8 MMb/d.

Vessel traffic monitored by EDA along the Gulf Coast decreased W-o-W. There were 25 vessels loaded for the week ending May 3, and 21 vessels the prior week. EDA expects US exports to be 4.3 MMb/d.

The SPR awarded contracts for 3.2 MMbbl to be delivered in April 2024. The SPR has 366.9 MMbbl in storage as of May 3, 2024.

Regulatory and Tariffs

Presented by ARBO

Tariffs:

Capline Pipeline Company LLC A new incentive program was established for deliveries of light crude petroleum oil, only applying to deliveries of at least 45 Mb/d through December 31, 2026. (FERC No 2.6.0 IS24- 261, filed April 130, 2024)

Gray Oak Pipeline, LLC Initial rates were established for qualifying alternative shipments originating from Helena West, Karnes County, TX to Pawnee Station (Sugarloaf), Bee County, TX and from Pawnee Station to Corpus, Nueces County, TX or Ingleside, San Patricio County, TX. The initial rates were established per the terms of the TSA and agreed to by at least one non-affiliated shipper. (FERC No. 2.81.0 IS24- 259, filed April 29, 2024

The above information is provided by ARBO’s Oil Pipeline Tariff Monitor. For more information on regulatory proceedings or tariff rates, please contact please contact Corey Brill via email at corey@goarbo.com or phone at 202-505-5296. https://www.goarbo.com/

-1.png)