Executive Summary: Rigs: The total US rig count decreased by 7 rigs for the April 28 week, down to 574 from 581. Infrastructure: The much-anticipated start of the Trans Mountain expansion project (TMX) became a reality on May 1, adding 590 Mb/d of egress capacity from the Western Canadian Sedimentary Basin (WCSB). Storage: East Daley expects an injection of 369 Mbbl in commercial and Strategic Petroleum Reserve (SPR) inventories for the week ending May 10.

Rigs:

The total US rig count decreased by 7 rigs for the April 28 week, down to 574 from 581. Liquids-driven basins drove the decline, down 8 rigs W-o-W to a total of 467. The Permian and Eagle Ford basins each lost 3 rigs, with the Permian losses coming from the Delaware. The DJ decreased by 2 rigs W-o-W to 8.

In the Delaware, operators EOG Resources, Occidental, and Avant Operating each subtracted one rig from their systems. Crescent Energy, EOG Resources, and Rosewood operating in the Eagle Ford each removed one rig from their systems. Chevron and Verdad Resources each took away one rig.

Infrastructure:

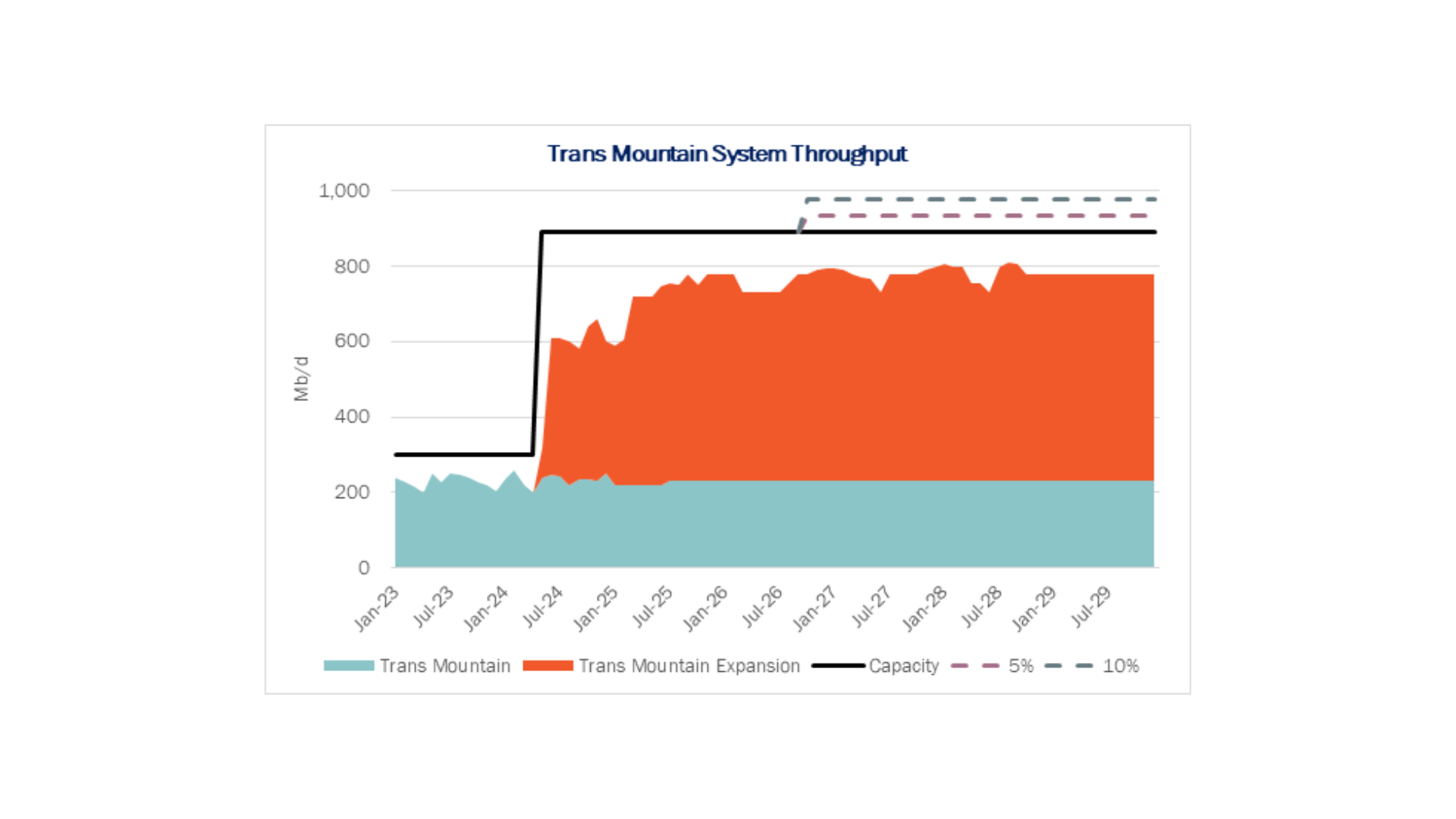

The much-anticipated start of the Trans Mountain expansion project (TMX) became a reality on May 1, adding 590 Mb/d of egress capacity from the Western Canadian Sedimentary Basin (WCSB). With deliveries to TMX starting, Canadian producers are optimistic that direct access to export markets will elevate the historically discounted Western Canadian Select (WCS) price for heavy sour oil from the oil sands.

The WCSB produces an important barrel for US refiners. About 70% (2.92 MMb/d) of the crude imported from Canada is a heavy sour barrel primarily sold as refinery feedstock. That heavy sour barrel (~20 API gravity) cannot be replaced with growth from the Permian Basin, which yields a light sweet oil with >50 API gravity.

US refineries are primarily equipped to refine heavier crude barrels of a sour quality (i.e. at least 0.5% sulfur content). The average crude oil input to refineries is a sour barrel with a 33 API gravity and 1.3% sulfur content. To optimize refinery performance and balance abundant US light crude production, 91% of US crude oil imports have an API gravity under 35.

As TMX continues to gain momentum and reach minimum volume commitments of 470 Mb/d by 3Q24, East Daley believes volumes initially will come from Enbridge’s (ENB) Mainline, TC Energy’s (TRP) Keystone, and Express Pipeline (ENB). By YE24, our forecast shows Canadian production growing by 295 Mb/d and beginning to replace WCSB barrels lost to the Gulf Coast. EDA expects Canadian production will grow by ~500 Mb/d by YE25 and into 1Q26, thus filling the egress created by TMX and bringing pipes from the WCSB to over 90% utilization. Additionally, all volumes initially moved to TMX will be replaced on Enbridge Mainline, Express and Keystone.

Storage:

East Daley expects an injection of 369 Mbbl in commercial and Strategic Petroleum Reserve (SPR) inventories for the week ending May 10. We expect total US stocks, including the SPR, will close at 829 MMbbl.

The US natural gas pipeline sample, a proxy for change in oil production, fell ~1.51% W-o-W across all liquids-focused basins. Samples decreased 7.22% in the Rockies and 7.10% in the Eagle Ford. The declines were offset by a 3.08% increase in the Anadarko, 1.36% in the Barnett, and 0.78% in the Permian. Both the Williston Basin and the Rockies have a very high correlation between gas volumes and crude oil volumes, whereas the Eagle Ford’s correlation is less than 30%. We expect US crude production to remain flat at 13.1 MMb/d.

According to US bill of lading data, US crude imports decreased by 219 Mb/d W-o-W to 6.7 MMb/d. More than 60% of the supply originated from Canadian pipelines into the US, with the remainder largely coming from ships carrying crude from Mexico, Brazil and Argentina.

As of May 10, there was ~561 Mb/d of refining capacity offline, including downtime for planned and unplanned maintenance. EDA expects gross crude inputs into refineries to increase by ~307 Mb/d W-o-W, coming in at 16.2 MMb/d.

Vessel traffic monitored by EDA along the Gulf Coast decreased W-o-W. There were 27 vessels loaded for the week ending May 10 and 25 the prior week. EDA expects US exports to be 3.9 MMb/d.

The SPR awarded contracts for 3.1 MMbbl to be delivered in May 2024. The SPR has 368 MMbbl in storage as of May 3, 2024.

Regulatory and Tariffs:

Presented by ARBO

Tariffs:

TransCanada Keystone The temporary discounted uncommitted rates were extended through June 30, 2024.(FERC No 6.98.0 IS24- 257, filed April 29, 2024)

Marketlink, LLC The volume incentive rates were decreased for the month of May, 2024. (FERC No. 3.24.0 IS24- 256, filed April 29, 2024

The above information is provided by ARBO’s Oil Pipeline Tariff Monitor. For more information on regulatory proceedings or tariff rates, please contact please contact Corey Brill via email at corey@goarbo.com or phone at 202-505-5296. https://www.goarbo.com/

-1.png)