Executive Summary: Rigs- The US rig count increased by 5 W-o-W with total rigs settling at 594. Infrastructure- Shell Wins Big in GoM Oil and Gas Lease Sale. Storage - East Daley expects a draw of 2,100 MMbbl in commercial and SPR inventories for the week ending Dec 29. We expect total US stocks, including the SPR, will close at 789.601 MMbbl. Tariffs - West Texas Gulf Pipe Line Company LLC established rules & rates for uncommitted and committed volumes for movements from Colorado City, Scurry County, Texas and Midland, Midland County, Texas to Sour Lake, Hardin County, Texas. (IS24- 91, filed December 1, 2023)

Rigs:

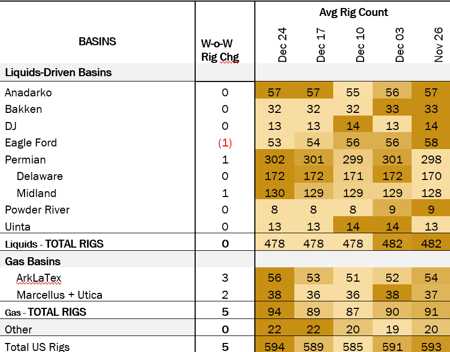

The US rig count increased by 5 W-o-W with total rigs settling at 594.  Liquid basins remained flat W-o-W with the count holding at 478. The Midland Basin gained 1 rig and the Eagle Ford lost 1 rig while all other basins held steady and saw no change. Mewbourn Oil gained 1 rig in the Delaware Basin. In the Eagle Ford Verdun Oil Company and Magnolia Oil and Gas each lost one rig while EOG Resources gained 1.

Liquid basins remained flat W-o-W with the count holding at 478. The Midland Basin gained 1 rig and the Eagle Ford lost 1 rig while all other basins held steady and saw no change. Mewbourn Oil gained 1 rig in the Delaware Basin. In the Eagle Ford Verdun Oil Company and Magnolia Oil and Gas each lost one rig while EOG Resources gained 1.

Infrastructure:

Shell Wins Big in GoM Oil and Gas Lease Sale

On December 20th, the Bureau of Ocean Energy Management reported 26 companies participated in the Gulf of Mexico Oil and Gas lease sale 261, submitting 352 bids totaling $442 million. The sale generated $382 million for 311 tracts across 1.7 million acres.

Shell was the big winner, acquiring 65 blocks, totaling 420,480 acres across several areas including Alaminos Canyon, Mississippi Canyon, Green Canyon, Atwater Valley and Keathley Canyon.

Hess acquired 20 blocks, totaling 126,720 acres, 16 of which are in the Green Canyon area. Chevron acquired 18 blocks in the East Breaks Area, totaling 184,320 acres.

Repsol acquired 29 blocks in the Mustang Island Area and another 7 in the Matagorda Island Area, totaling 226,223 acres. Repsol also won 50% stake in 3 other blocks with Talos Energy. Talos Energy reported that it had acquired 13 blocks, or about 74,000 acres. Separately Talos Energy announced that it was executing Lease Exchange agreements with BP, Chevron, and Hess to consolidate acreage across 15 blocks in the Green Canyon area.

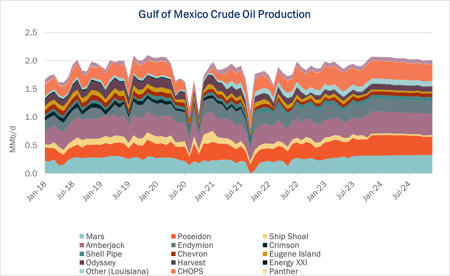

East Daley forecasts offshore production by pipeline, breaking out volumes delivered to Houston and Louisiana. In December 2023, we estimate ~0.4 MMb/d were delivered to Houston, the majority on Genesis's (GEL) Cameron Highway Offshore Pipeline System (CHOPS). CHOPS currently delivers an estimated 0.3 MMb/d, operating at just 53% utilization. We expect deliveries on the pipeline to grow to ~0.46 MMb/d by the end of 2025. CHOPS is fed by several smaller GEL pipes which aggregate volumes from the Green Canyon and Keathley Canyon areas.

Most of the Gulf's crude volumes end up in Louisiana serving refinery demand, ~1.54 MMb/d in September '23, the latest month for which we have reported volumes. East Daley forecasts Louisiana offshore crude supply to grow to ~1.64 MMb/d by the end of 2025, as new deepwater acreage is developed. We anticipate the majority of these volumes to show up on Shell's Amberjack pipeline, which is currently operating at ~60% capacity.

Storage:

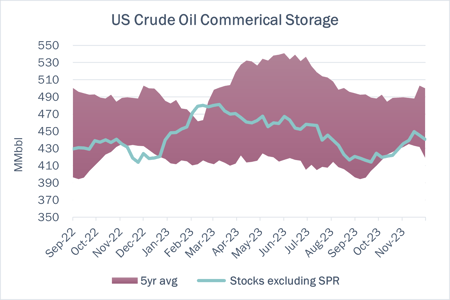

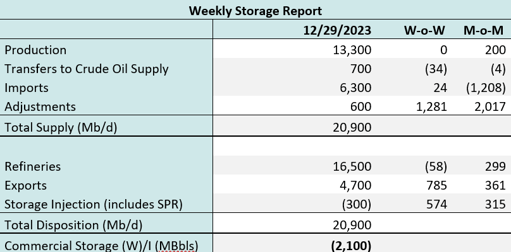

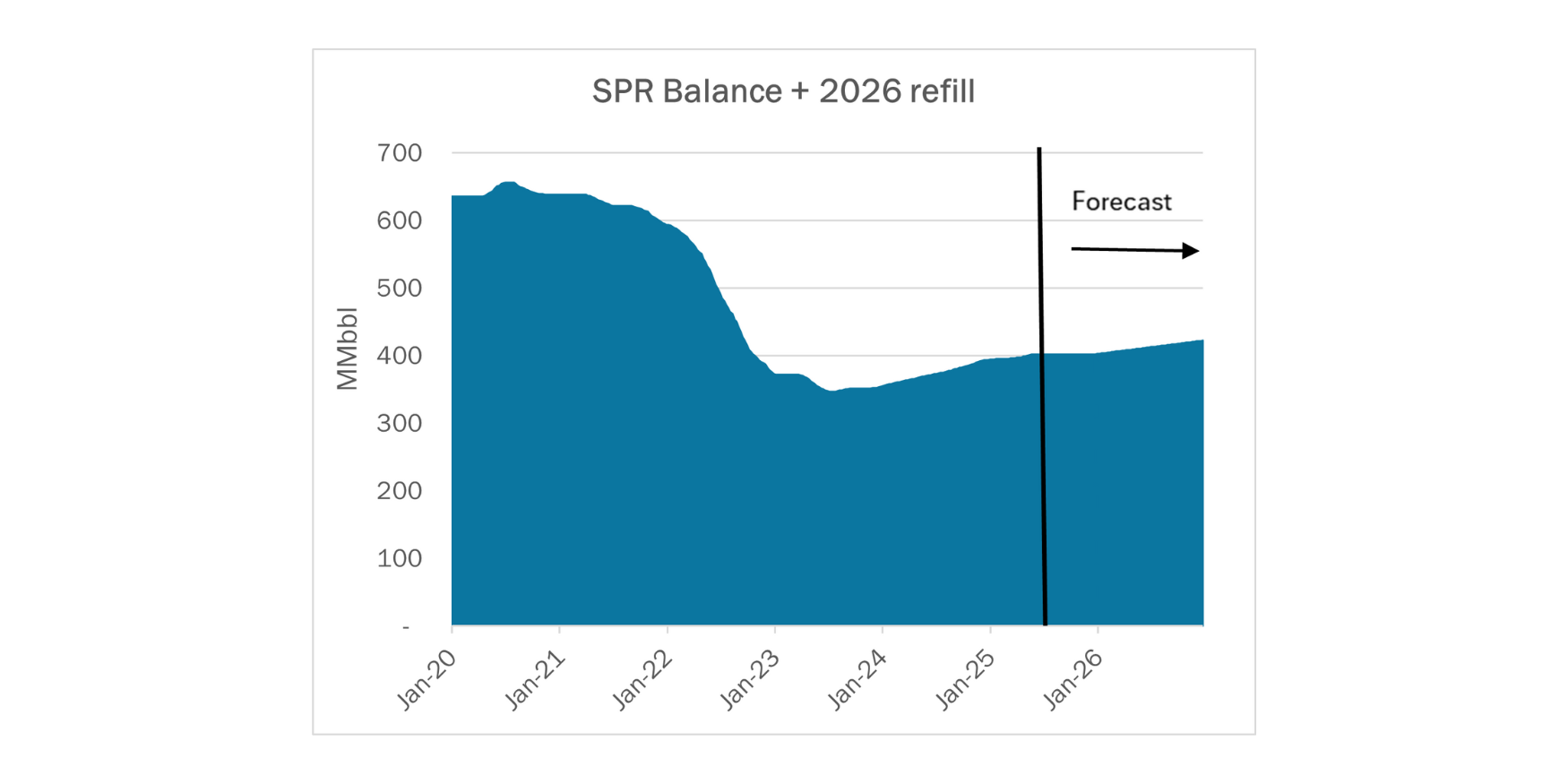

East Daley expects a draw of 2,100 MMbbl in commercial and SPR inventories for the week ending Dec 29. We expect total US stocks, including the SPR, will close at 789.601 MMbbl.

The US natural gas pipeline sample, a proxy for change in oil production, increased by 0.28% in liquids-focused basins. The Gulf of Mexico saw a significant change, gaining 2.25% W-o-W and the Permian gained 1.3% W-o-W. The Gulf of Mexico has a high pipeline sample coverage, however the Permian pipeline sample is less than 42%. We expect US crude production to be flat at 13.3 MMb/d.

According to US bill of lading data, US crude imports increased slightly by ~24 Mb/d W-o-W to 6.3 MMb/d. More than 60% of the supply originated from Canadian pipelines into the US, with the remainder largely coming from ships carrying crude from Mexico and Nigeria.

As of December 15, there was ~106 Mb/d of refining capacity offline, including downtime for planned and unplanned maintenance. EDA expects gross crude inputs into refineries to decrease by .4% W-o-W, coming in at ~16.5 MMb/d.

Vessel traffic monitored by EDA along the Gulf Coast decreased W-o-W. There were 28 vessels loaded for the week ending December 30 and 27 the prior week. EDA expects US exports to be 4.7 MMb/d.

The Strategic Petroleum Reserve, SPR, awarded contracts for 2.73 MMbbl to be delivered to Big Hill SPR site in January 2024. The SPR also saw a 793 MMbbl storage injection the week ending December 22 which East Daley believes to be part of a 2 MMbbl restock delivered throughout Dec 2023.

Regulatory and Tariffs

Presented by ARBO

Tariffs:

West Texas Gulf Pipe Line Company LLC established rules & rates for uncommitted and committed volumes for movements from Colorado City, Scurry County, Texas and Midland, Midland County, Texas to Sour Lake, Hardin County, Texas. (IS24- 91, filed December 1, 2023)

TransCanada Keystone Pipeline, LP has increased rates on the variable portion of the committed rate structure as a result of estimated changes in its operating, maintenance and administration costs for 2024. All Shippers have agreed to the rates for Port Arthur and Houston. Permanent diversion rates were also increased. The temporary discounted Uncommitted Rates were extended through January 31, 2024. (IS24-75 filed November 30, 2023)

The above information is provided by ARBO’s Oil Pipeline Tariff Monitor. For more information on regulatory proceedings or tariff rates, please contact please contact Corey Brill via email at corey@goarbo.com or phone at 202-505-5296. https://www.goarbo.com/

-1.png)