Crude Oil Edge: November 29, 2023

Rigs:

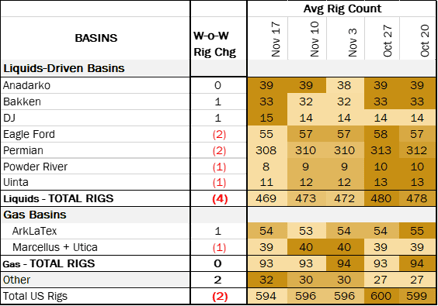

The US rig count decreased by 2 W-o-W to bring the total count to 594. Liquids basins lost 4 rigs, including 2 rigs in the Eagle Ford, 2 in the Permian, 1 in the Powder River and 1 in the Uinta basins. The Bakken and DJ basins each gained 1 rig while the Anadarko held steady with no change.

In the Permian Basin, Diamondback Energy (FANG) added 2 rigs, Devon Energy (DVN) added 1, while ConocoPhillips (COP), Endeavor and Coterra Energy (CTRA) each dropped 1 rig. Overall, public operators in the Permian dropped 2 rigs while privates added 2. Enerplus added 1 rig in the Bakken, and Verdad gained 1 in the DJ. Rockies Resources Holdings shed 1 rig in the Powder River and Uinta Wax Operating dropped 2 in the Uinta Basin.

Infrastructure:

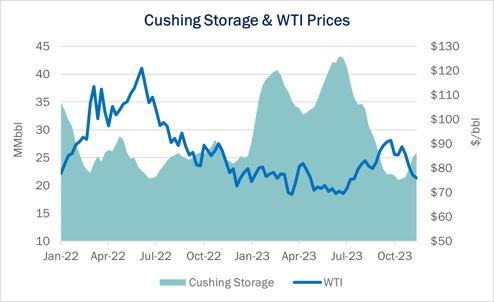

Cushing storage is a key fundamental indicator for US crude oil prices, as seen in the benchmark WTI (West Texas Intermediate) price for a physical barrel at Cushing. As demand for barrels grows and storage is depleted, the price of oil usually goes up. However, in 2023 Cushing storage levels have changed by ~30% in either direction while WTI prices have remained more steady at about a +/- 10% variance.

WTI rose by 10% as Cushing storage levels fell in September 2023, but then fundamentals and prices seemed to disconnect. WTI prices started declining even as inventory at Cushing inventory continued to fall to a 5-year low of 21 MMbbl in October. Other US crude oil fundamentals include record production of 13.2 MMb/d, while crude exports have averaged 4.1 MMb/d, well above the 5-year average of 3.1 MMb/d. Strong demand and historically low storage inventory would normally push WTI higher, but prices have fallen instead.

East Daley believes recent WTI price weakness is related to uncertainty over global demand, including slowing growth in China and the risk of a recession in many markets. Supply risk in the Middle East from the Israel-Hamas conflict also has receded. Meanwhile, OPEC’s continued production cuts and Russian oil sanctions have failed to reverse this bearish trend.

The Cushing hub in Oklahoma is the heart of the US crude oil market, providing physical delivery for the Nymex WTI futures contracts. Cushing has immense infrastructure including over 25 inbound and outbound pipelines, numerous pipelines to refineries, and 16 major storage terminals.

Cushing has 94 MMbbl of total tank storage capacity and 78 MMbbl of working capacity, according to the Energy Information Administration (EIA). Cushing connects more than 4 MMb/d of North American production from the Western Canadian Select Basin (WCSB), Bakken, Niobrara, Powder River, and Denver-Julesburg to Midwest and Gulf Coast refineries and export docks. Cushing is unrivaled in its optionality and ability to segregate, batch and blend production to react to market conditions and meet refiners’ needs.

Storage:

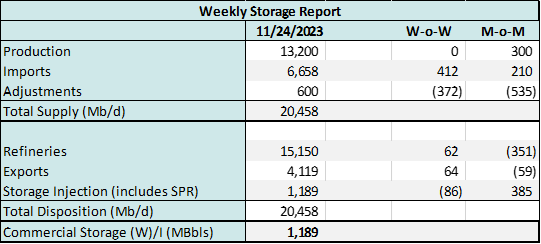

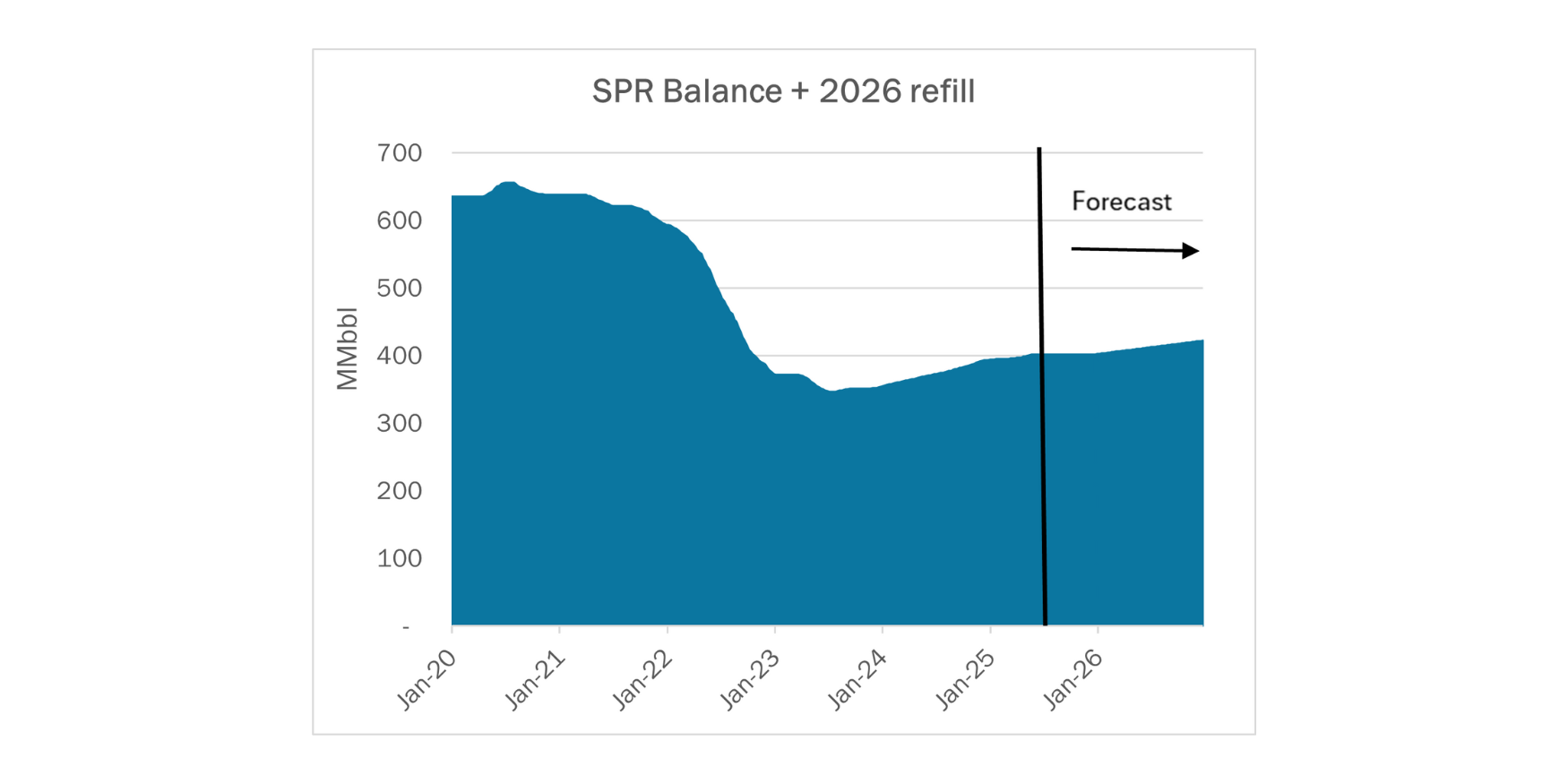

East Daley expects an injection of 1.2 MMbbl in commercial inventories for the week ending November 24. We expect total US stocks, including the SPR, to close at 800.5 MMbbl.

The US natural gas pipeline sample, a proxy for change in oil production, increased by 0.6% in liquids-focused basins. The Williston Basin gained 4% W-o-W, whereas the Texas Gulf and Gulf of Mexico saw a 4.7% and 5.4% reduction W-o-W, respectively. The Gulf of Mexico and Williston Basin have high pipeline sample coverage. We expect US crude production to remain flat at 13.2 MMb/d.

According to US bill of lading data, US crude imports decreased by ~21 Mb/d W-o-W to 6.7 MMb/d. More than 60% of the supply originated from Canadian pipelines into the US, with the remainder largely coming from ships carrying crude from Mexico, Argentina and Brazil.

As of November 24 there was ~0.35 MMb/d of refining capacity offline, including downtime for planned and unplanned maintenance. EDA expects gross crude inputs into refineries to decrease by 0.1% W-o-W to ~15.15 MMb/d.

Vessel traffic monitored by EDA along the Gulf Coast decreased W-o-W. There were 28 vessels loaded for the November 17 week vs 21 vessels the prior week. EDA expects US exports to be 4.1 MMb/d.

Regulatory and Tariffs

Presented by ARBO

Tariffs:

TransCanada Keystone Pipeline, LP (TRP) will be raising the uncommitted International Joint Tariff (IJT) rates from Hardisty, AB, to Port Arthur and Houston, TX. The 11% rate increase, to be effective December 1, 2023, will remain less than the sum of the local tariff component rates and does not affect any other posted rate. (IS24- 16, filed October 30, 2023)

Additionally, TransCanada Keystone Pipeline will extend its temporary discounted rates through December 31, 2023. The discounted rate equates to a discount in the ceiling level of uncommitted rates from the international boundary at or near Haskett, Manitoba to Patoka, Houston or the US Gulf Coast. (IS24- 14, filed October 30, 2023)

The above information is provided by ARBO’s Oil Pipeline Tariff Monitor. For more information on regulatory proceedings or tariff rates, please contact please contact Corey Brill via email at corey@goarbo.com or phone at 202-505-5296. https://www.goarbo.com/

-1.png)