Natural Gas Weekly: April 13, 2023

Flows – West Coast storage facilities exited winter at the lowest inventory level in 22 years, setting the stage for higher regional demand and prices in 2023.

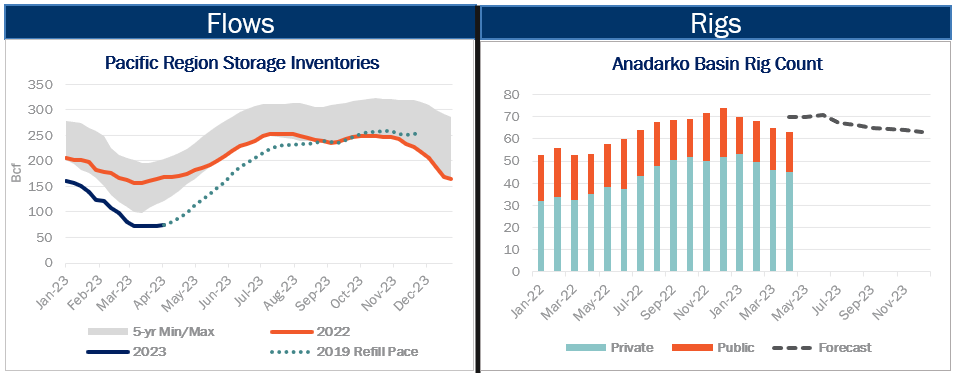

Working gas inventory in the Pacific region fell to 72 Bcf in mid-March, according to EIA’s storage survey, the lowest in weekly regional estimates dating to 2010. EIA’s state-level monthly storage data shows inventories on the West Coast (California, Oregon and Washington) reached an historic low of 68 Bcf in February 2021 amid the 2000-01 California energy crisis.

In contrast to other regions, the West Coast has experienced below-normal weather during the 2022-23 heating season, including a series of powerful storms that created an historic snowpack in California. Cumulative gas-weighted heating degree days (GWHDDs) through the end of March were 16% above normal in the Pacific region, according to National Weather Service data, resulting in strong demand for heating and power generation.

East Daley Analytics covers the West Coast in our US Macro Supply and Demand Forecast, as well as pipeline flows to the West in the Rockies and Permian Supply and Demand forecasts. Pacific region storage totaled 74 Bcf in EIA’s latest survey for the April 7 week, 56% lower than last year and 57.5% below the 5-year average for this time of year.

Low inventory will result in more demand from regional utilities to refill storage ahead of next winter. The last significant storage rebuild in the Pacific region occurred in 2019; if storage facilities refill at the same pace this year, then regional inventory would return to normal seasonal levels by October.

The dynamic should support a West Coast market premium this year. Higher prices are drawing volumes from as far away as the Northeast via the Rockies Express Pipeline, and regional prices must stay elevated to attract the marginal molecule. Operators in basins that directly feed the West Coast, including the Permian, Rockies and Western Canada, stand to benefit the most.

Rigs – Rig activity in the Anadarko Basin has tapered off recently in response to lower commodity prices. The basin has shed 8 rigs since the end of January, declining to 63 total rigs in April. Private operators account for most of the change, dropping 7 of the 8 rigs since January.

The rig decline will have minimal impact on East Daley’s basin-level forecast for 2023, as shown in our Production Scenario Tools. Adjusting our March and April rig counts down by 5 rigs in the Anadarko Basin generates a drop of 45 MMcf/d in 2023 production. East Daley expects Anadarko rig activity will continue to slowly decline this year based on the WTI price curve, with additional downside risk possible if natural gas prices stay lower.

Infrastructure – Waha gas prices are feeling the pressure from pipeline maintenance in the Permian Basin. Waha spot prices fell below $1/MMBtu this week as maintenance on Gulf Coast Express (GCX) and Permian Highway Pipeline (PHP) continue.

East Daley recently flagged the likelihood of volatility in April due to pipeline downtime. According to informational postings, GCX expects the maintenance to last until Saturday (April 15), reducing pipeline capacity to 1.6 Bcf/d. PHP also updated its customers this week, stating that shipping restrictions should be lifted by April 14. Capacity on PHP has been reduced to 1.6 Bcf/d during the maintenance event.

Storage – EIA reported a 25 Bcf storage withdrawal for the April 7 week, putting working gas inventory at 1,855 Bcf. In our updated Macro Supply and Demand Forecast, we estimate working gas ends April at 2,103 Bcf. US storage is 295 Bcf above the 5-year average after the latest EIA report.

Natural Gas Weekly

East Daley Analytics’ Natural Gas Weekly provides a weekly update to our monthly Macro Supply and Demand Forecast. The update covers rigs, flows, production, prices and capacity constraints that materially change our view on supply and demand. This update highlights what investors and traders need to monitor in natural gas to ensure they are on the right side of the market. Subscribe to the Natural Gas Weekly.