The Daley Note: March 1, 2023

Energy Transfer (ET) released earnings on Feb. 15, and while the company beat both East Daley and consensus expectations, 2023 guidance came in well below our forecast. We trace the discrepancy to ET’s exposure to falling natural gas prices.

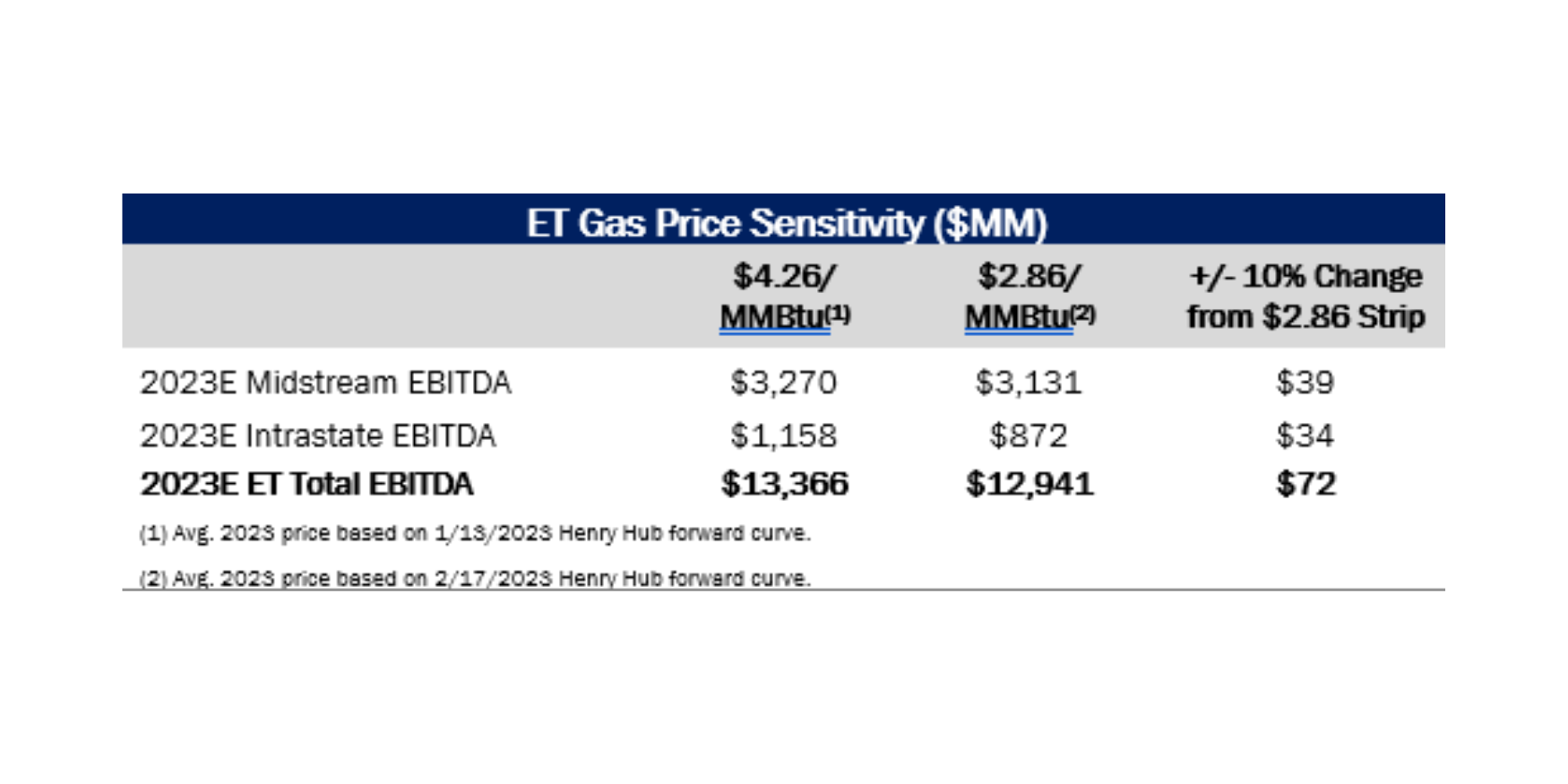

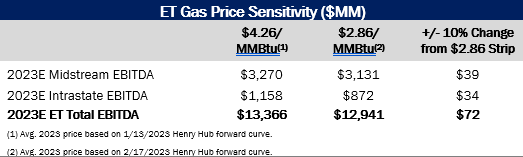

ET guided to 2023 Adj. EBITDA of $12.9-$13.3 billion, well below East Daley’s estimate of $13.4 billion in our company Financial Blueprint. Our forecast was based on our last Blueprint model released mid-January, when the forward Henry Hub price still averaged $4.26/MMBtu for 2023.

Henry Hub futures have fallen sharply in 2023 on a combination of mild winter weather and strong supply growth. As of Feb. 17, the forward curve averaged $2.86/MMBtu for the year, a 33% drop from our mid-January update ahead of the 4Q22 report.

By rolling the new strip into our ET Blueprint, the -33% change in commodity prices only results in a -3% change in EBITDA for Energy Transfer. However, that equates to a whopping $425 million drag for the midstream giant, bringing our EBITDA forecast down to $12.9 billion, at the low end of management’s guidance (see table). From the current level, a 10% change in gas prices can have a +/- $72 million impact on ET’s 2023 EBITDA.

Almost all of the financial impact is in the company’s Intrastate Gas and Midstream segments. The Intrastate segment is where ET conducts most of its natural gas marketing. Despite the relatively wide Waha-Katy basis, the lower Henry Hub price curve has erased almost $250 million from our Natural Gas Sales margin forecast in 2023.

The Midstream segment is primarily impacted by the commodity exposure from the acquired Enable Midstream (ENBL) assets. Our 2023 forecast for the ENBL Anadarko system, which we estimate is ET’s second-largest system by EBITDA, declined by $50 million given its high commodity exposure (~30-40%) through percent-of-proceed (POP) contracts. Our forecast for ET’s ENBL Haynesville asset also declined by $30 million due to lower fuel fees.

Even with lower natural gas prices, we expect ET to return to growth in 2024 as new projects and production growth start to offset the price impacts. The company has a new NGL fractionator coming online in 3Q23, two new Permian gas processing plants, and latent capacity on its Lone Star NGL pipeline. The Crude segment should also benefit as volumes on its Permian Express pipelines recover and marketing earnings improve. In the near term, however, prices may prove to be too much of a headwind. — Ajay Bakshani, CFA Tickers: ET.

Dirty Little Secrets: After Hours – The Natural Gas Undoing Project

East Daley hosted a webinar on Thursday, Feb. 23 to look deeper into the natural gas story. In “Dirty Little Secrets: After Hours – The Natural Gas Undoing Project,” East Daley explored the short- and long-term supply and demand factors driving natural gas prices. Are market risks being accurately priced in the forward curve? When will more LNG demand arrive? East Daley explores the dynamics driving the natural gas market. Click here to see a recording of “The Natural Gas Undoing” webinar.

Stay Ahead of the Market with Natural Gas Weekly

East Daley Analytics’ Natural Gas Weekly provides a weekly update to our monthly Macro Supply and Demand Forecast. The update covers rigs, flows, production, prices and capacity constraints that materially change our view on supply and demand. This update highlights what investors and traders need to monitor in natural gas to ensure they are on the right side of the market. Contact us for more information on Natural Gas Weekly.

The Daley Note

Subscribe to The Daley Note (TDN) for midstream insights delivered daily to your inbox. The Daley Note covers news, commodity prices, security prices and EDA research likely to affect markets in the short term.