Executive Summary: Markets: Mont Belvieu and Conway propane prices diverged from late February to April on tariff-related volatility. Rigs: The total US rig count decreased by 2 during the week of May 4 to 546. Liquids-driven basins decreased by 7 W-o-W from 452 to 445. Flows: For the week ending May 22, US natural gas volumes averaged 70.3 Bcf/d in pipeline samples, marking a W-o-W increase from 69.5 Bcf/d the previous week Calendar: Ethane S&D, Propane S&D – 5/26

Infrastructure:

Mont Belvieu and Conway propane prices diverged considerably from late February to April on volatility connected to the US-China trade spat. The spread normally trends around $0.05 or below, but blew out to over $0.25 when Mont Belvieu spot propane prices surged to $0.97/gal in late April.

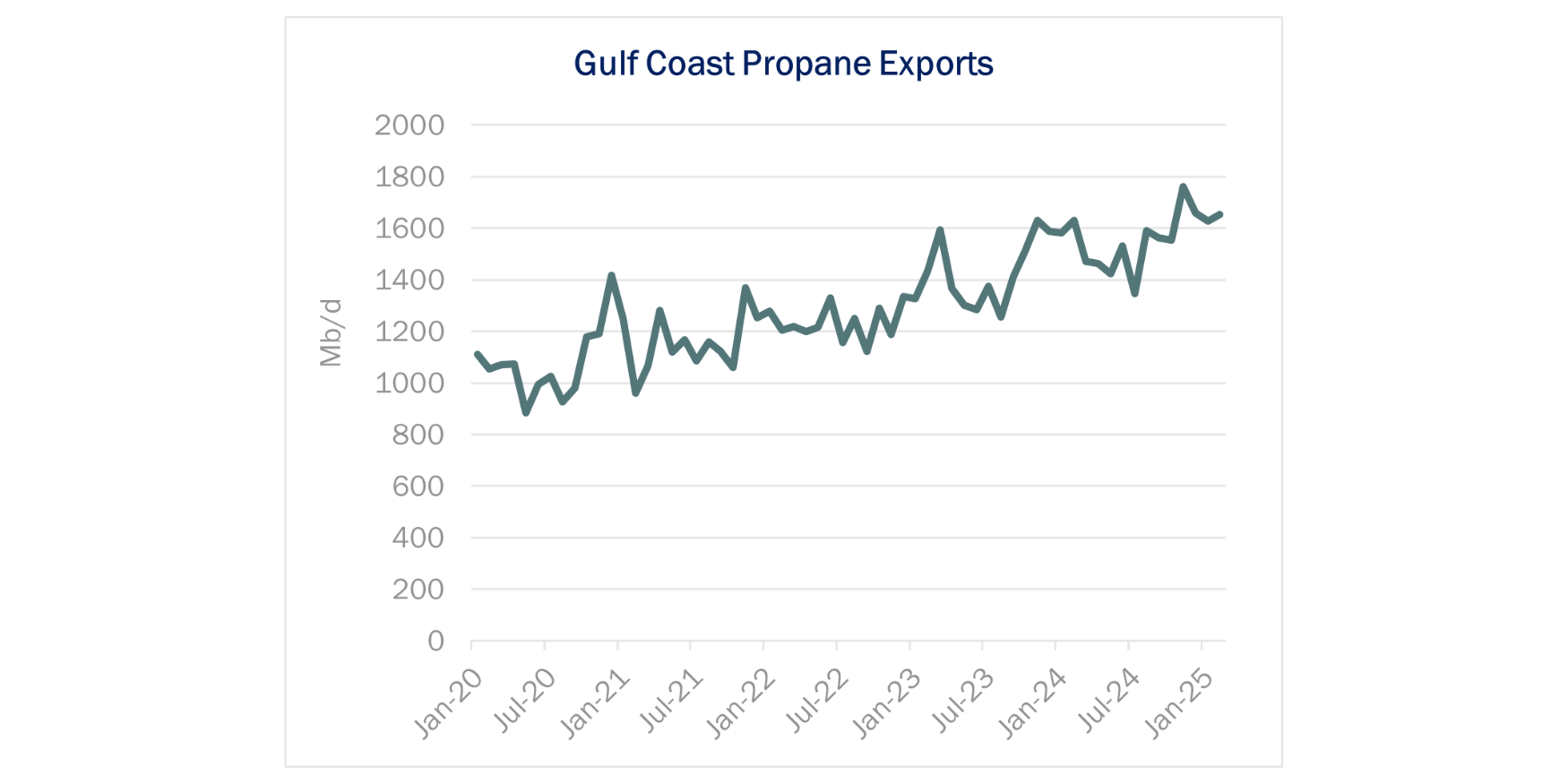

The trade dispute between Beijing and Washington appears to have contributed to the dislocation. Gulf Coast propane exports were strong in 1Q25, reaching near-record levels in February ’25 of 1.65 MMb/d, according to the latest Energy Information Administration (EIA) data (see figure). The trade fight began that same month, when President Trump set a 10% tariff on imports from China starting February 4, and Beijing immediately retaliated with its own tariffs on US goods. China is the largest market for US propane, and petrochemical buyers may have accelerated their purchasing as relations soured.

Robust exports combined with more normal heating demand led propane inventory to fall sharply over the winter. The chart below shows EIA data for finished propane stocks in PADD 3 (Gulf Coast) storage facilities. Inventory fell to a low of 11.8 MMbbl for the week ending April 11, 39% below a year ago. Companies report that LPG export demand held strong at terminals in April, bucking fears of a slowdown as the US-China trade war escalated. With limited demand coverage in storage and April turning out to be a strong export month, prices shot higher for Mont Belvieu propane.

The Conway-Mont Belvieu spread is now back within normal levels, but East Daley will continue to monitor propane inventory at Mont Belvieu for further volatility.

Rigs:

The total US rig count decreased by 2 during the week of May 4 to 546. Liquids-driven basins decreased by 1 W-o-W from 446 to 444.

- Permian-Midland (-1): Diamondback Energy

- Permian-Delaware (-1): EOG Resources

- Anadarko (+2): Blackbeard Operating, Darrah Oil

- Bakken (-2): ConocoPhillips, Silver Hill Energy

- DJ (-1): Creek Road Miners

- Eagle Ford (-1): SM Energy

Flows: For the week ending May 22, US natural gas volumes averaged 70.3 Bcf/d in pipeline samples, marking a W-o-W increase from 69.5 Bcf/d the previous week.

Liquids-driven basins increased 0.6 Bcf/d to 18.7 Bcf/d. The Permian Basin increased 7% W-o-W to average 6.2 Bcf/d, with the Delaware Basin increasing 8% to 5 Bcf/d.

Gas-driven basins were relatively flat W-o-W, averaging 44 Bcf/d. The Haynesville increased by 2% from 10.4 Bcf/d to 10.6 Bcf/d. The Marcellus+Utica remain relatively flat on a W-o-W.

Looking ahead, the Appalachia and Haynesville basins will be pivotal to monitor. With increased demand on the horizon, we expect increased production from these regions will be critical to maintain a balanced market.

Calendar:

-1.png)