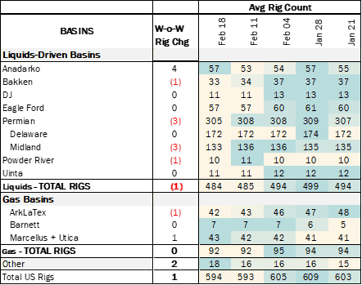

Executive Summary: Rigs: US rig activity was flat in liquids-driven basins, losing 1 rig overall. Infrastructure: The price spread from Midland to the Magellan East Houston (MEH) market is primed to gap out in 2024, according to flows predicted in the Crude Hub Model. Storage: East Daley expects a build of 3.85 MMbbl in commercial and Strategic Petroleum Reserve (SPR) inventories for the week ending March 1.

Rigs:

US rig activity was flat in liquids-driven basins, losing 1 rig overall. However, there were notable changes within basins as the Anadarko gained 4 rigs while the Delaware Basin lost 3 rigs. The Powder River Basin lost 1 rig. The DJ, Eagle Ford, Midland and Uinta basins all remained flat with no change in rig counts.

Anadarko producers Presidio Petroleum, Calcuta Petroleum and Shelby Resources each added 1 rig. Texland Petroleum and Triple Crown Resources both dropped 1 rig in the Midland Basin, and EOG Resources dropped 1 rig in the Powder River Basin.

Infrastructure:

The price spread from Midland to the Magellan East Houston (MEH) market is primed to gap out in 2024, according to flows predicted in the Crude Hub Model. While we don’t expect the spread to open up like the ~$12/bbl blowout seen in 2018, regional price volatility should increase. East Daley forecasts the MEH-Midland spread to increase by ~185%; from ~$0.70 to ~$2.00/bbl in 2024.

As Permian crude oil production continues to grow, pipeline takeaway will begin to tighten. East Daley’s Crude Hub Model forecasts Permian egress to exceed 80% utilization by July 2024. As pipe capacity grows more scarce, Midland prices will come under pressure, causing the spread to widen.

EDA forecasts the MEH-Midland spread to reach ~$2.00/bbl, as the lion’s share of the remaining egress routes run to Cushing. For a Permian barrel to reach the Gulf Coast via Cushing, it must first travel north to Cushing and then south to the Houston/Nederland markets, incurring additional tariffs. The barrel will also likely lose its premium as a ‘pure Permian’ crude quality due to extensive blending at Cushing.

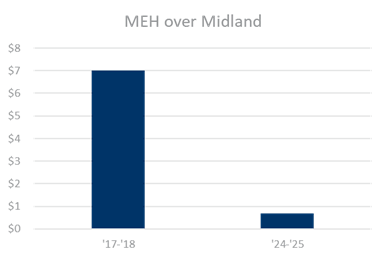

The 2018 MEH spread blowout was mainly due to pipeline constraints. As Permian egress approached 80% utilization in 2018, MEH prices averaged $7+/bbl over Midland. Available pipeline space at the time averaged ~460 Mb/d.

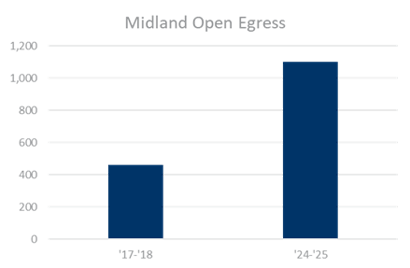

EDA forecasts pipe utilization to cross 80% once again this year, in July 2024. Currently the forward MEH-Midland spread is averaging $0.70/bbl, or ~$6.00 lower than in 2017-18. One key difference is there is more overall capacity available after the construction of several greenfield pipelines. The Crude Hub Model forecasts available pipeline capacity to average ~1,100 Mb/d in 2H24, more than double the available egress in 2017 and 2018.

We expect MEH-Midland volatility to pick up in 2024, and we will keep a close eye on 2026 and 2027 for potentially bigger swings.

The Permian Basin saw strong growth in 2023, and East Daley’s Production Scenario Tools forecast the Permian to grow another 6% through 2024. The bulk of this supply growth will take place in 2H24 at 245 Mb/d of incremental volume, ending the year at 6.5 MMb/d of production.

Storage:

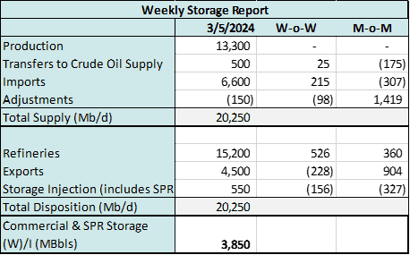

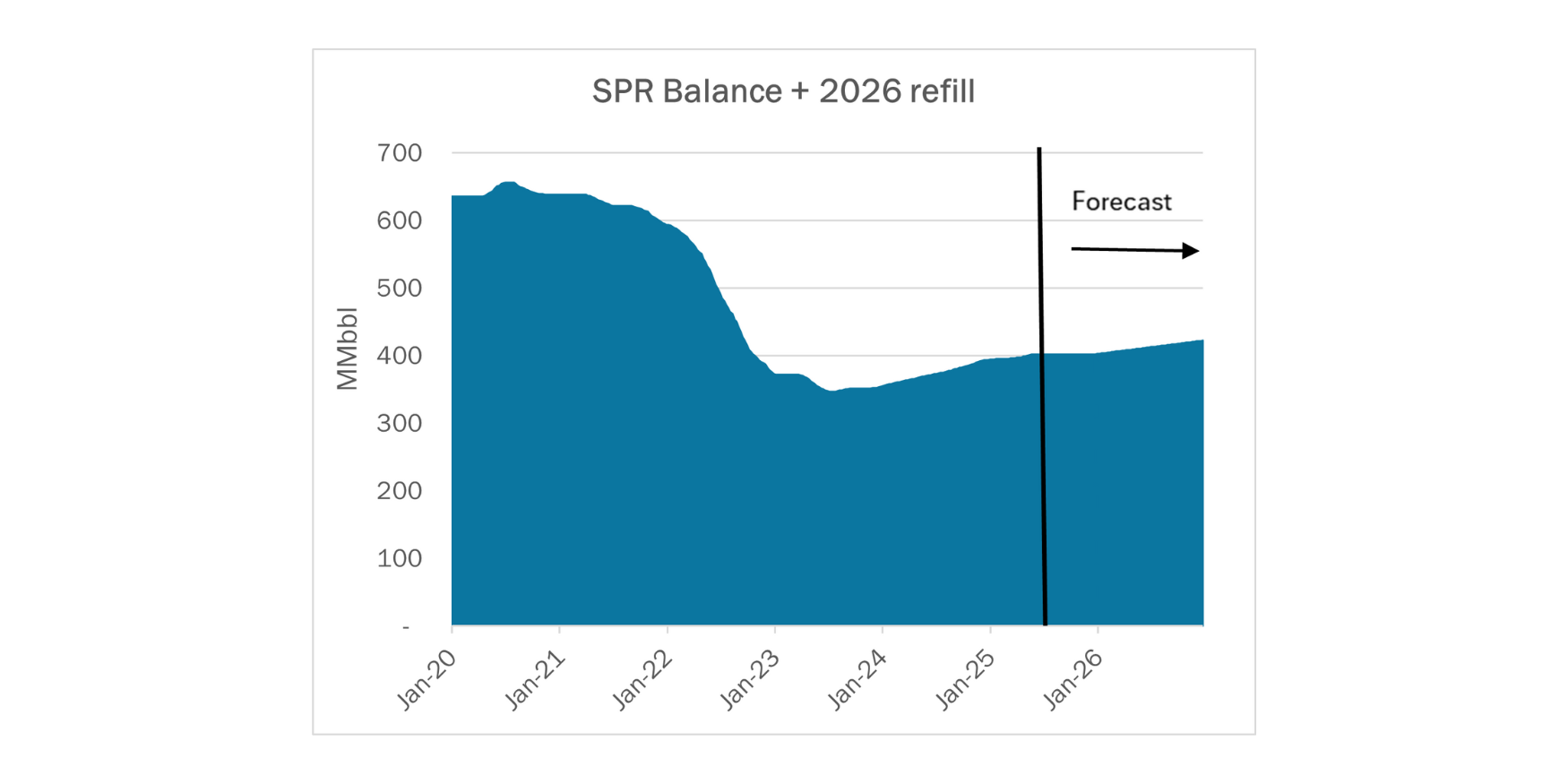

East Daley expects a build of 3.85 MMbbl in commercial and Strategic Petroleum Reserve (SPR) inventories for the week ending March 1. We expect total US stocks, including the SPR, will close at 811.267 MMbbl.

The US natural gas pipeline sample, a proxy for change in oil production, decreased by 1.0% in liquids-focused basins, driven by a reduction of 3.4% in the Eagle Ford and 2.6% in the Uinta. We expect US crude production to remain at 13.3 MMb/d.

According to US bill of lading data, US crude imports decreased by ~215 Mb/d W-o-W to 6.6 MMb/d. More than 60% of the supply originated from Canadian pipelines into the US, with the remainder largely coming from ships carrying crude from Mexico, Nigeria and South America.

As of March 4, there was ~697 Mb/d of refining capacity offline, including downtime for planned and unplanned maintenance. EDA expects gross crude inputs into refineries to increase by ~526 Mb/d W-o-W, coming in at 15.2 MMb/d.

Vessel traffic monitored by EDA along the Gulf Coast decreased W-o-W. There were 24 vessels loaded for the week ending March 2, and 27 the prior week. EDA expects US exports to be 4.5 MMb/d.

The SPR awarded contracts for 2.99 MMbbl to be delivered in March 2024. The SPR has 360.3 MMbbl in storage as of February 23, 2024.

Regulatory and Tariffs

Presented by ARBO

Tariffs:

Seaway Crude Pipeline Company LLC announced it is extending the incentive rates through March 31, 2024. The incentive rates are applicable to shippers with volumes of 10,000 b/d or more. (FERC No 2.82.2 IS24- 195, filed February 15, 2024, 2024)

The above information is provided by ARBO’s Oil Pipeline Tariff Monitor. For more information on regulatory proceedings or tariff rates, please contact please contact Corey Brill via email at corey@goarbo.com or phone at 202-505-5296. https://www.goarbo.com/

-1.png)