Natural Gas Weekly: May 5, 2023

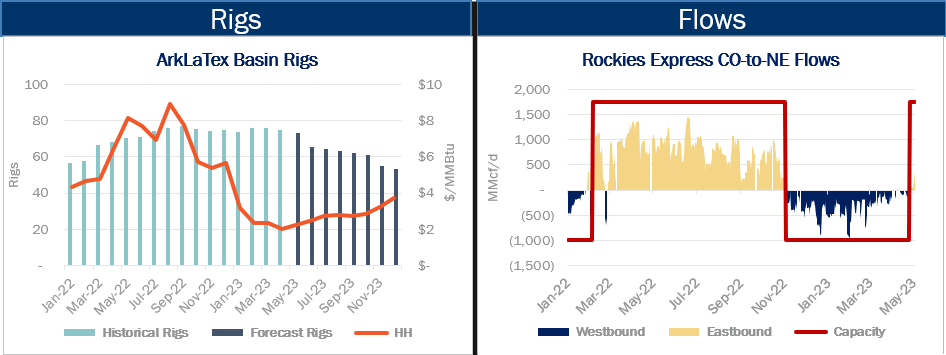

Rigs - Haynesville producers continue to guide to relatively modest pullbacks in drilling and completion work later this year. Comstock Resources (CRK), Chesapeake (CHK) and Southwestern Energy (SWN) reported 1Q23 earnings this week, and guidance was consistent with 4Q22 reports three months ago.

CHK reiterated its plan to trim its Haynesville program in Louisiana and East Texas from 6 rigs to 5 in 2023. The producer says it will release the rig in 3Q23. CHK also plans to drop one frac crew from the ArkLaTex Basin in 2Q23. CHK currently operates 13 rigs across the US.

Comstock said it intends to drop 1-2 rigs in the next few weeks from its legacy Haynesville program, but will continue delineating its Western Haynesville play with 2 rigs in 2023. CRK guided to 14 wells drilled by YE23 in the exploratory Western Haynesville, which has yielded several impressive wells. CRK said it is currently running 6-7 rigs on its legacy acreage.

Southwestern stuck to guidance for a 7-8 rig Haynesville program during 2023. SWN said it is delaying completion activity on its dry gas acreage and will release a frac fleet in 2Q23. The producer is guiding to a modest impact on its production in 2H23 and a flatter quarterly production forecast.

East Daley remains underwhelmed by guidance to date in the ArkLaTex Basin for a course correction. In the Balanced scenario of our Macro Supply and Demand Forecast, ArkLaTex rig counts must begin dropping soon to avoid an oversupply problem later this year. We estimate Haynesville rig counts to fall by ~10 rigs in 2Q23, sliding toward 60 rigs this summer. Yet rig counts have been holding steady in the mid-70s, according to East Daley's Energy Data Studio, delaying a material shift.

We also expect operators to begin stockpiling drilled but uncompleted wells (DUCs). Updated guidance from SWN and CHK would be consistent with this trend. Will it be enough to stave off oversupply this year? Much will depend on weather, LNG exports, and the strength of power generation demand, variables we will continue to track in our Macro Supply and Demand Forecast.

Flows - Westbound flows on Rockies Express Pipeline (REX) from the Midwest to Colorado have reversed this week as shoulder-season demand in the Pacific and Mountain West regions requires less gas. REX is currently shipping 300 MMcf/d from Colorado toward the Midwest market, the first eastbound flows on REX since early November 2022.

Midwest storage inventories started refilling in mid-April after EIA posted an 18 Bcf build for the week ending April 21. REX is now flowing east and west out of the Cheyenne Hub, based on East Daley’s measurement of flows. REX is still delivering about 250 MMcf/d to Overthrust in the Western Rockies; the null point on REX has shifted to the Denver-Julesburg Basin as heating demand on Colorado’s Front Range has waned.

Pacific region storage inventories will continue to draw REX gas west this spring and summer to help refill record-low inventories. However, the forward curve for NWPL-Rockies basis has decreased by more than $1.00/MMBtu over the past month for the 2024 calendar due to easing concerns on West Coast supply and demand fundamentals. The region should benefit this year from strong hydroelectric generation this year and full service on the El Paso system’s Line 2000 from the Permian Basin. Line 2000 came back online in February 2023 after an 18-month outage.

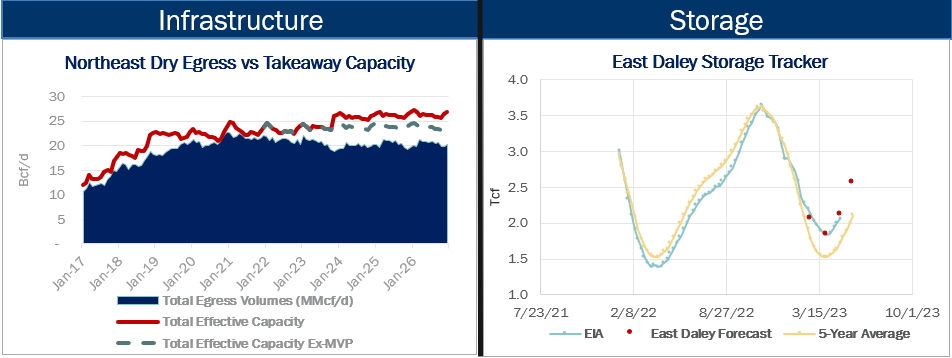

Infrastructure - Equitrans Midstream (ETRN) believes the Mountain Valley Pipeline (MVP) could still begin service in 2023 despite recent legal setbacks. In its 1Q23 earnings, ETRN acknowledged it still lacks permits, but said it can finish the pipeline in under six months once it is allowed to resume construction. Legal issues have delayed the project and continue to create uncertainty.

MVP was dealt a blow in April when the Fourth Circuit vacated the water quality certification issued by the West Virginia Department of Environmental Protection (DEP). ETRN management believes the WV DEP will be able to adequately address the Fourth Circuit’s concerns and allow the pipeline to move forward. MVP is also awaiting permits to cross the Jefferson National Forest, which management expects to have in hand by the end of May. East Daley now models MVP to start in 4Q24.

Storage - EIA reported a 54 Bcf storage injection for the April 28 week, putting working gas inventory at 2,063 Bcf. In our updated Macro Supply and Demand Forecast, we estimate working gas ends April at 2,103 Bcf. US storage is 341 Bcf above the 5-year average after the latest EIA report.

Natural Gas Weekly

East Daley Analytics' Natural Gas Weekly provides a weekly update to our monthly Macro Supply and Demand Forecast. The update covers rigs, flows, production, prices and capacity constraints that materially change our view on supply and demand. This update highlights what investors and traders need to monitor in natural gas to ensure they are on the right side of the market. Subscribe to the Natural Gas Weekly.

-1.png)