Natural Gas Weekly: March 16, 2023

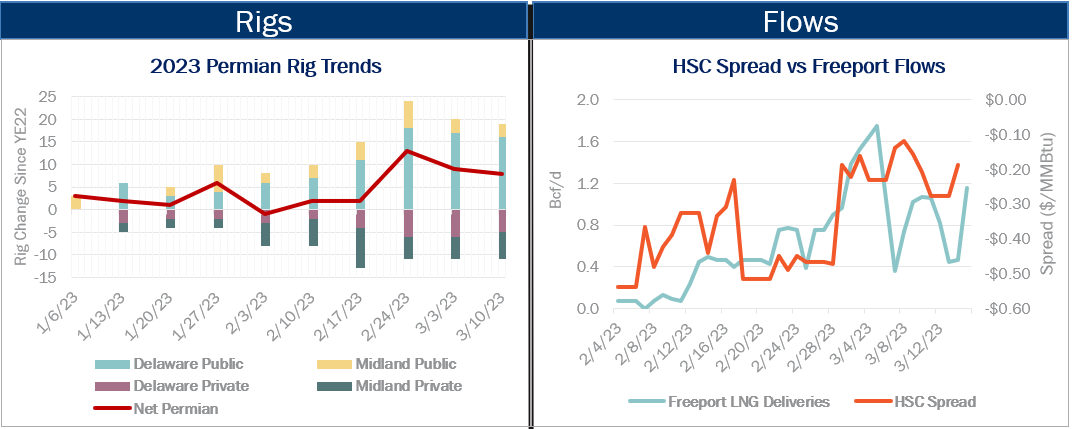

Rigs - Public and private producers are taking divergent paths in the Permian Basin so far in 2023. The overall basin rig count has increased by 2% (+8 rigs) year to date, totaling 338 rigs for the March 10 week, according to Blackbird BI data. However, the mix between public and private rig counts has shifted more drastically. The largest change has been in the Delaware sub-basin, where public operators have added 16 rigs in 2023, growing from 100 to 116 rigs (+16%), while private E&Ps have dropped 5 rigs. The same trends are apparent in the Midland, where public producers have added 3 rigs while their private counterparts have dropped 6 rigs. Overall, rigs run by private Permian drillers have declined by 7%, from 162 rigs to 151 rigs.

Flows - The restart of Freeport LNG is helping firm up natural gas prices at the Houston Ship Channel (HSC). Pipeline deliveries to Freeport began to ramp in mid-February following regulatory approval to resume partial commercial service, reaching a high of ~1.75 Bcf/d on March 5. The spread between HSC and the Henry Hub prices narrowed over this period, from a discount of $0.50/MMBtu in early February to a $0.20-0.30 discount this week, according to Bloomberg price data. The spread was as narrow as $0.12 on March 8.

The additional demand from Freeport, located on Quintana Island south of Houston, has helped prices strengthen along the industrial corridor. Freeport received regulatory approval on March 8 to restart Train 1, the last of the three liquefaction trains at the facility to receive approval. Feedgas flows remain variable as Freeport continues to test equipment and resume operations, totaling 1.15 Bcf/d as of March 15.

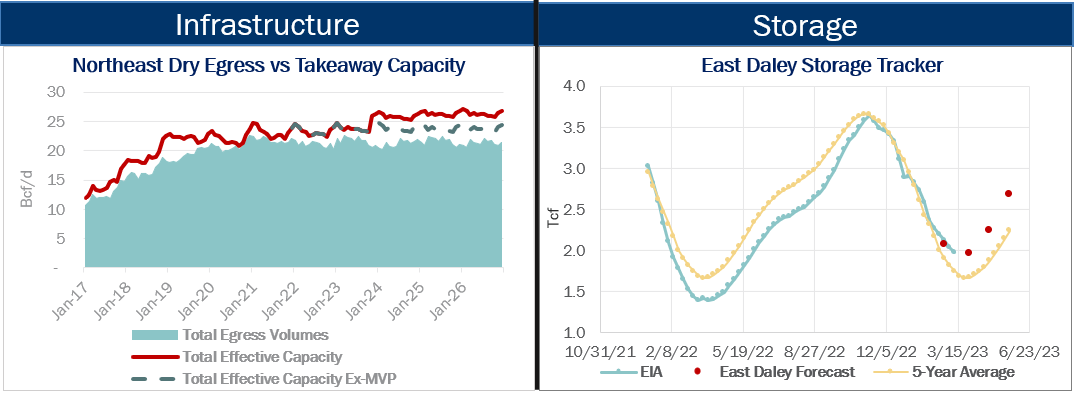

Infrastructure - Mountain Valley Pipeline (MVP) scored a major permitting win earlier this month, securing a Biological Opinion from the US Fish and Wildlife Service. The progress opens a window for the long-delayed pipeline to finish permitting and potentially complete construction by YE23, according to lead developer Equitrans Resources (ETRN). MVP is still waiting on individual water crossing permits from the Army Corps of Engineers. Management expects to have those permits by mid-April. MVP is also awaiting permits to cross the Jefferson National Forest in Virginia, which management expects to have in hand by the end of May.

MVP is no longer as critical to the near-term supply outlook in our Northeast Supply and Demand Forecast gave relatively flat production in the Marcellus and Utica shales, but the success of the project would allow for more long-term growth as demand expands from LNG projects on the Gulf Coast.

Storage - EIA reported a 58 Bcf storage withdrawal for the March 10 week, putting working gas inventories at 1,972 Bcf. In our Macro Supply and Demand Forecast, we estimate storage inventories end March at 1,965 Bcf. Storage is 378 Bcf above the 5-year average after the latest EIA report.

Natural Gas Weekly

East Daley Analytics' Natural Gas Weekly provides a weekly update to our monthly Macro Supply and Demand Forecast. The update covers rigs, flows, production, prices and capacity constraints that materially change our view on supply and demand. This update highlights what investors and traders need to monitor in natural gas to ensure they are on the right side of the market. Subscribe to the Natural Gas Weekly.

-1.png)