Executive Summary:

Infrastructure: Keyera becomes an NGL powerhouse after acquiring Plains All American’s (PAA) Canadian assets.

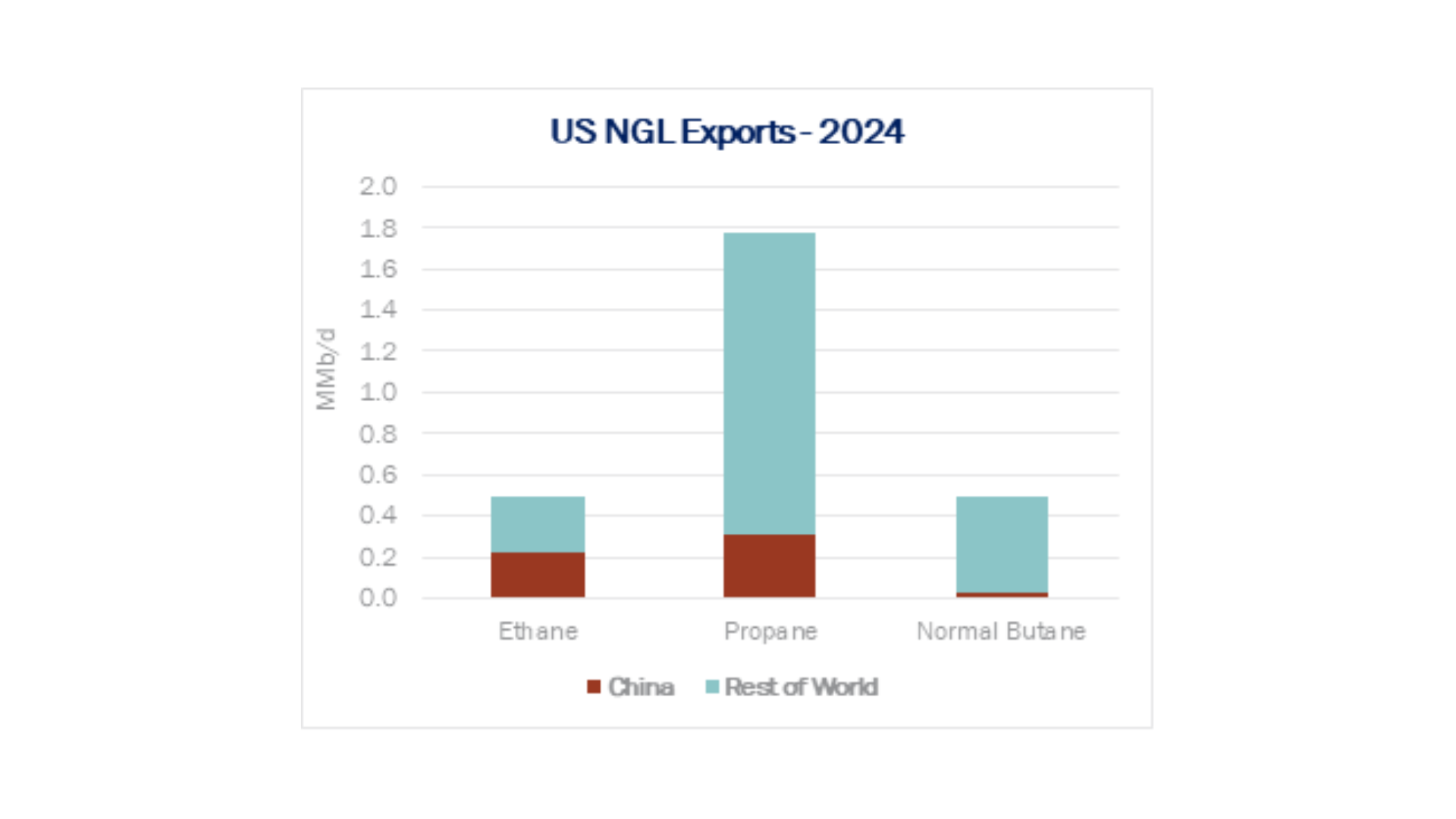

Exports: LPG exports surged 20% W-o-W, by contrast ethane exports fell 56% W-o-W.

Rigs: The US rig count decreased during the week of June 1 to 523. Liquids-driven basins decreased by 3 W-o-W from 416 to 413.

Flows: US natural gas volumes averaged 69.5 Bcf/d in pipeline samples for the week ending June 15, down 0.4% W-o-W from 69.8 Bcf/d the previous week.

Calendar: Purity Product Forecast & Ethane SD & Propane SD & *NEW Butane SD – 6/27

Infrastructure:

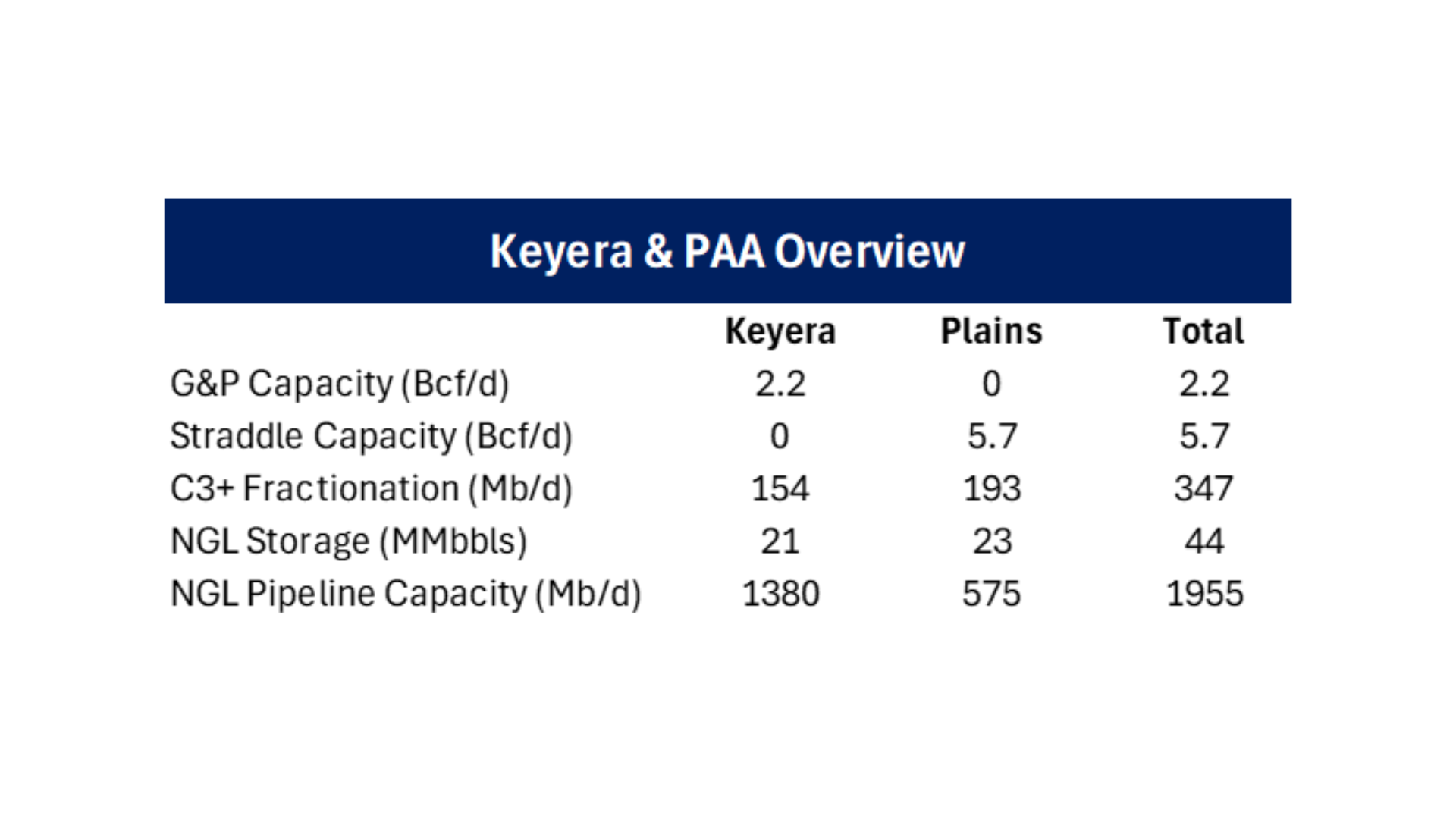

Keyera’s (KEY.TO) C$5.15B acquisition of Plains All American’s (PAA) Canadian NGL assets transforms it into a coast-to-coast powerhouse with arguably the most flexible NGL platform in Canada.

By adding ~193 Mb/d of fractionation capacity and 23 MMbbl of cavern storage across Fort Saskatchewan and Sarnia, Keyera can offer producers and marketers full-service logistics from northeastern British Columbia to Eastern Canada. The deal also contributes 5.7 Bcf/d of straddle plant capacity at Empress and a critical Y-grade pipeline network, putting Keyera in direct competition with Pembina (PBA) for NGL transport and fractionation services. PAA and Keyera expect to close the transaction in 1Q26.

While Pembina remains dominant at Alberta’s core NGL hub — with Redwater’s capacity soon hitting 256 Mb/d and 21 MMbbl of integrated storage — Keyera will challenge that leadership in scale and redundancy. PBA still has the edge in long-haul liquids pipelines (~1.1 MMb/d across Peace and Northern), but Keyera’s KAPS system (~175 Mb/d and expanding into northeastern BC) offers strong Montney connectivity and is already ~75% contracted under long-term take-or-pay contracts. With both firms positioned at Edmonton/Fort Saskatchewan, customer decisions may hinge on service bundling, pricing and downstream access.

AltaGas, meanwhile, is carving out a different lane entirely. Its dominant West Coast export footprint — RIPET and Ferndale today, REEF by 2026 — makes it the LPG egress leader. Unlike KEY or PBA, AltaGas controls over 70 Mb/d of LPG export capacity and is vertically integrating upstream with Pipestone and North Pine. Notably, AltaGas has inked an 18-year deal to lease frac space at Keyera’s KFS, hinting at greater midstream cooperation as Montney propane volumes surge.

The PAA deal grows Keyera from a regional midstreamer to a national NGL integrator combining scale, geography and flexibility. While PBA still leads on pipeline and storage depth, and AltaGas leads at the dock, Keyera now offers a credible “best-of-both-worlds” platform. Its next test: execution. If Keyera can integrate Plains’ assets and optimize east-west flows while leveraging AltaGas’ terminals, it may become Canada’s most versatile NGL operator.

Exports:

LPG exports surged 20% W-o-W, led by a 216% spike in volumes out of PSX Freeport and a 40% increase from ET Marcus Hook. The gains suggest stronger terminal throughput and potential one-off vessel timing effects.

Ethane exports, by contrast, fell 56% W-o-W, with volumes down from both ET Nederland and EPD Morgan’s Point. While ET’s Orbit facility remains anchored by Satellite Chemical (STL), export approvals appear to be a constraint—STL has placed cargoes with Reliance Industries in India but continues to face challenges securing ethane export permits.

Rigs:

The total US rig count decreased during the week of June 1 to 523. Liquids-driven basins decreased by 3 W-o-W from 416 to 413.

- Permian (-1):

-

- Delaware (-6): Vital Energy, Permian Resources, Matador Resources, Coterra Energy (-2), Spur Energy

-

- Midland (+5): Vital Energy (+2), Occidental Petroleum, Double Eagle, Red Tail Exploration

- Bakken (-2): Hess, Chord Energy

- Uinta (+2): Uinta Wax Operating, Anschutz

- Anadarko (-1): Validus Energy

- Powder River (-1): Anschutz

Flows:

US natural gas volumes averaged 69.5 Bcf/d in pipeline samples for the week ending June 15, down 0.4% W-o-W from 69.8 Bcf/d the previous week.

Gas-driven basins declined 0.4% W-o-W to average 44.1 Bcf/d. The Haynesville sample declined 2.9% to 10.6 Bcf/d. The Marcellus+Utica gained 0.2% to 32.8 Bcf/d.

Liquids-driven basins decreased 0.3% to 18.0 Bcf/d. The Eagle Ford sample held flat while Permian gas declined 0.5% to 5.8 Bcf/d.

Calendar:

-1.png)