Natural Gas Weekly: April 20, 2023

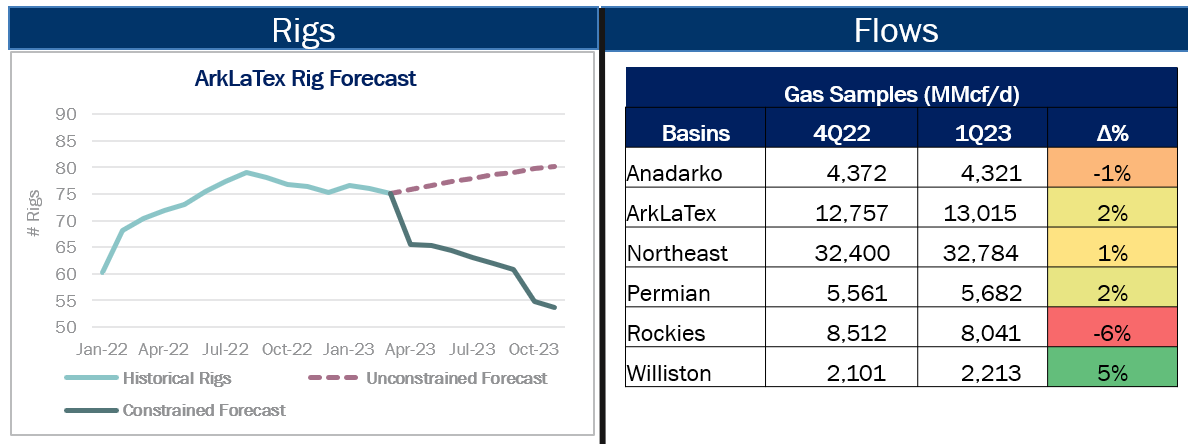

Rigs - Rig activity is holding steady in the Haynesville shale despite headwinds from $2/MMBtu natural gas, defying East Daley's expectations for a drilling slowdown.

The combination of production growth and a mild winter has the gas market contending with oversupply in 2023. East Daley expects the ArkLaTex Basin to play a key role in restoring balance as producers slow drilling and completion activity. Leading Haynesville producers Chesapeake Energy (CHK) and Comstock Resources (CRK) have guided to lower rigs this year, confirming our forecast for a decline in the basin.

Yet so far, there's not much evidence of any change in course. Haynesville rig counts in East Texas and northern Louisiana have averaged 76 so far in 2023 and held at 74-76 rigs in April, according to Blackbird BI data.

In the Balanced scenario of our Macro Supply and Demand Forecast, ArkLaTex rig counts must begin dropping soon to avoid an oversupply problem later this year. We estimate Haynesville rigs to fall by ~10 rigs in 2Q23 from current activity, sliding toward a count of 60 rigs this summer to help balance season-ending storage inventories.

With rigs holding strong, operators can also stockpile drilled but uncompleted wells (DUCs). Our Balanced scenario in the Macro Supply and Demand Forecast includes a hefty DUC build this year in the ArkLaTex. EIA's "Drilling Productivity Report" estimates Haynesville producers added 11 DUCs in February and 12 DUCs in March, confirming a slowdown in completions has started in the gas basin.

Flows - 1Q23 pipeline samples show higher gas production Q-o-Q in most basins, a positive indicator for midstream companies headed into earnings season.

Most basins show recovery from Winter Storm Elliot, which moved through the Lower 48 in December and cut into 4Q22 supply. We saw a drop in pipeline gas samples across the US as the cold front descended from the north, with recovery following in most basins in 1Q23. The Bakken region, which was heavily affected by the weather, rose 5% Q-o-Q in the 1Q23 samples, averaging 2.2 Bcf/d. Samples for the Permian Basin hit a record high in March, rising 2% for the quarter to average 5.7 Bcf/d.

The Rockies basins bucked the positive overall trend, declining 6% Q-o-Q. The region saw a cold winter that likely caused some freeze-offs to linger, but supply is on the way to fully recovering, finishing the quarter at 8 Bcf/d. Basins have different coverage rates in the gas samples, but the real-time data allows us to closely monitor production trends.

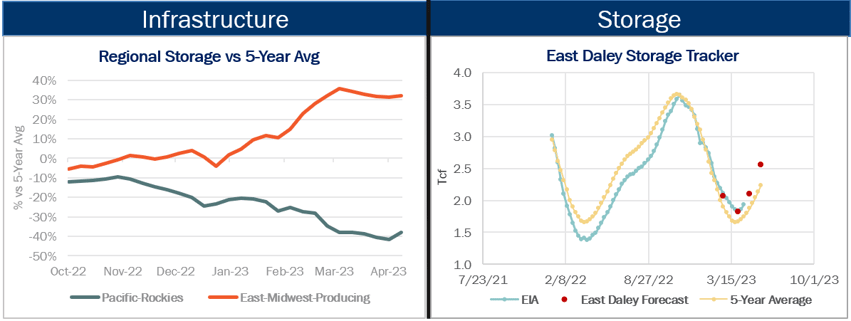

Infrastructure - An unusual winter weather pattern has created an East-West division in the natural gas market.

The US saw winter temperatures 6% above normal through the end of March, according to gas-weighted heating degree days (GW-HDD) measured by the National Weather Service (NWS). Behind this national trend was a balmy season featuring record warmth across many eastern US markets, while the West Coast and Rocky Mountains experienced a cold winter. According to NWS census data, the New England (-13%), mid-Atlantic (-14%) and Southeast (-14%) regions saw GW-HDDS fall well below normal, while cumulative GWHDDs were 16% above normal in the Pacific region.

The result is a bifurcated gas market based on regional storage. Inventory in the West (Pacific and Rockies) is 38% below the 5-year average in mid-April, according to EIA storage data, while working gas in the East (Midwest, Northeast and Producing Region) is 32% above 5-year norms. The divergence in storage should continue to support wider spreads between regional prices.

Storage - EIA reported a 75 Bcf storage withdrawal for the April 14 week, putting working gas inventory at 1,930 Bcf. In our updated Macro Supply and Demand Forecast, we estimate working gas ends April at 2,103 Bcf. US storage is 329 Bcf above the 5-year average after the latest EIA report.

Natural Gas Weekly

East Daley Analytics' Natural Gas Weekly provides a weekly update to our monthly Macro Supply and Demand Forecast. The update covers rigs, flows, production, prices and capacity constraints that materially change our view on supply and demand. This update highlights what investors and traders need to monitor in natural gas to ensure they are on the right side of the market. Subscribe to the Natural Gas Weekly.

-1.png)