Executive Summary: Rigs: The total US rig count decreased by 8 for the May 26 week, down to 563 from 571 rigs. Flows: The US interstate flow sample is down slightly W-o-W for the week of Jun 9. Infrastructure: Energy Transfer (ET) is looking to tap into the growing ethane market in the Northeast. Purity Product: Ethane demand saw a 61 Mb/d boost in 1Q24 vs 4Q23.

Rigs:

The total US rig count decreased by 8 for the May 26 week, down to 563 from 571 rigs. Liquids-driven basins drove the decline, down 5 rigs W-o-W to a total count of 458 from 463 the previous week. The Permian Basin count saw the largest loss, decreasing by 7 rigs W-o-W. The Bakken saw a loss of 1 rig. The Anadarko Basin increased by 2 rigs and the Eagle Ford gained 1 rig.

In the Bakken, operator True Companies dropped 1 rig. In the Permian, Delaware operators Occidental Petroleum, Exxon, Diamondback Energy and Permian Resources each removed 1 rig. Midland operators Diamondback Energy, Chevron and Triple Crown Resources also dropped 1 rig each. In the Anadarko Basin, Continental Resources and Blake Production added 1 rig each, and EOG Resources added 1 rig in the Eagle Ford.

Flows:

The US interstate flow sample is down slightly W-o-W for the week of Jun 9. Samples for liquids-focused basins declined 1.2% W-o-W, led by reductions in the Midland and Powder River basins. In the Powder River, maintenance on the Wyoming Interstate system is scheduled until June 13, which impacted flow volumes there by 10.6% W-o-W. In the Anadarko, the 4.5% decline in residue sample occurred on Northern Natural Gas where maintenance is expected for June. The NNG segment connected to the Spraberry station in the Midland is also undergoing maintenance from June 4-7.

The flow sample in gas-driven basins is also down slightly W-o-W. Producers in the ArkLaTex continue to curtail production due to low gas prices and delayed LNG demand. In the Northeast (Marcellus+Utica) supply has been increasing over the past few weeks as EQT has lifted production slightly, although the Northeast sample is flat W-o-W.

Infrastructure:

Energy Transfer (ET) is looking to tap into the growing ethane market in the Northeast. The company has reached an agreement with Rover Pipeline to build a ~400 MMcf/d interconnect with ET’s Revolution plant to extract more ethane from the gas stream.

Rover Pipeline has filed an application with FERC to build the interconnect in Washington County, PA to an ETC Northeast Pipeline straddle plant (ET’s Revolution plant). The interconnect will deliver ethane-rich gas to the Revolution plant where ET can use latent capacity to remove NGLs. The residue methane then will be reinjected back into Rover via the existing Rover-Revolution receipt meter. The interconnect with the Revolution plant is expected to be completed by 4Q24 and cost ~$4MM.

Downstream of the project, Rover primarily connects into MPLX’s gas processing plants and receives the largest ethane share (as a percentage of gas receipts) from MPLX’s Sherwood, Seneca and Cadiz plants, as well as Blue Racer’s Berne plant. MPLX recently expanded the Harmon Creek processing facility in February 2024 but did not expand its de-ethanization capabilities. The Harmon Creek meter on Rover has increased its ethane content percentage by ~2% from January-June ‘24. The proposed Revolution tie-in would be on the same Rover lateral connected to Harmon Creek.

The project has raised concerns among some Rover shippers. On April 15, BP Energy filed a protest to the Rover application, seeking clarity about how the “high-value” NGLs extracted from Rover will be allocated. Specifically, BP wants to know how shippers will be reimbursed and made whole for lost heating content that ET captures via the straddle plant. The time required to settle the dispute could put the project’s 4Q24 in-service at risk.

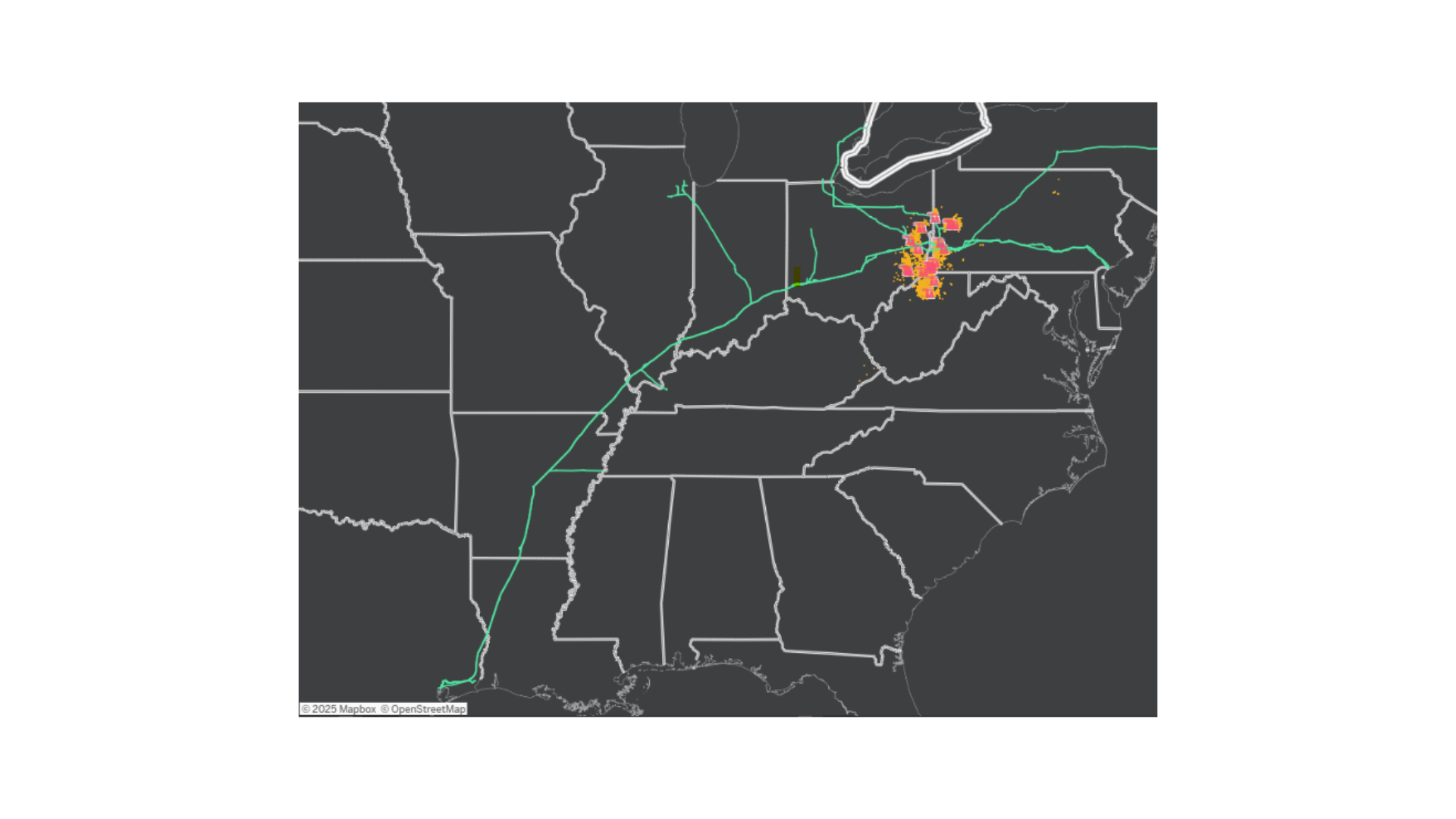

Mariner West (blue pipeline in map) and ME2X (green pipeline in map) are the two logical outlets for the extra ethane supply. ET owns both pipelines, as well as a 33% interest in Rover. EDA speculates the captured ethane would help support further refrigeration and storage capacity expansions at ET’s Marcus Hook ethane export dock. In EDA’s June Ethane Supply and Demand Report released last week, we forecast a 25 Mb/d increase in Marcus Hook dock capacity by July ’25. It’s possible ET has its eyes on more grandiose plans.

Purity Product Spotlight:

Ethane demand saw a 61 Mb/d boost in 1Q24 vs 4Q23. The graph below shows ethane volumes transported from MPLX’s Houston and Cadiz plants to Shell’s Monaco ethylene steam cracker via Shell’s Falcon pipeline. It is the highest recorded throughput on the pipeline feeding the steam cracker that has been beset by operational challenges. In February, Shell’s CEO Wael Sawan revealed the cracker cost $14B, far more than the original $6B estimate of capital costs. While two of the three polyethylene trains are operating at capacity, Sawan noted the cracker will not be fully online until ’25 or ’26. Falcon’s pipeline capacity is 107 Mb/d.

Release Calendar:

Release Calendar:

-1.png)